2026 Singapore Property Buying Guide: The Definitive Playbook for Buyers & Investors

– GOLD EDITION

By Sam Tan | Dunamis Property

Written for Singaporeans, by a Singaporean real estate advisor.

(All examples are for education only. Please check your own numbers before taking action.)

0. How to Use This Guide

This Gold Edition is the "full brain" version of the guide. It’s meant for serious buyers, HDB upgraders, and investors who don’t just want headlines but also the moving parts behind the 2026 window.

How to read this Gold Edition:

- If you’re an HDB upgrader: Read Sections 1 → 2 (macro), 3 (land cost), 5 (HDB), 8-9 (risk & safety nets), and 11.1 (case study).

- If you’re a first-time condo buyer or upgrader: Read Sections 1 → 2 (macro), 3 (land cost reset), 4 (rate & loan), 6 (condo buyers), 9, and 11.2.

- If you’re an investor: Read Sections 1 → 2 → 3, 4 (rates), 7 (investors), 8-9, and 11.3.

If you’re still unsure after reading, that’s normal. Use this guide to frame your questions, and then we can sit down and run through your numbers calmly together.

Throughout the guide, I’ll speak as one Singaporean to another straightforward, practical, and long-term minded.

If any term sounds technical, there’s a short Glossary at the back of this guide you can refer to.

Table of Contents

- 1. The 2026 Singapore Property Transition Window in One Page

- 2. From COVID to 2026: What Actually Changed in the Singapore Property Market?

- 3. New Launch Condo Prices: The "Old Land vs. New Land" Reset

- 4. Property Financing & Interest Rates: Pain, Relief, and Monthly Instalments

- 5. The HDB Double Wave: Sale Equity vs MOP Supply Through 2028

- 6. Safe Entry Math: Housing Ratio, Buffer and Layout Filters

- 7. Exit Planning for Second-Property Buyers: 7-10 Year Horizon

- 8. ABSD, TDSR & Policy Guardrails: "What If I'm Wrong?"

- 9. Property Financing Safety Nets & Affordability Rules

- 10. Singapore Property Buyer Psychology & Decision Traps

- 11. 2026 Decision Case Studies: HDB, First-Home, Second-Property

- 12. From Reading to Taking Action: Your Next Steps

- → Glossary – Key Terms

Dunamis Insight: My Take

When analyzing the 2026 Singapore property outlook, the biggest mistake I see buyers make is treating all real estate advice identically. You cannot apply an investor's framework to a first-time family home purchase, and vice-versa. That is why I broke this guide down by buyer profile. The market is stabilizing, and while the days of rapid, double-digit price jumps are cooling, the supply of new homes remains tight. This means your focus should not be on timing a market crash that is not coming, but on structuring for value based on your specific needs, affordability, and entry price. Whether that means a new launch or a solid resale unit, read the sections that matter to your life right now, ignore the noise, and let the data guide your next step.

1. The 2026 Singapore Property Transition Window in One Page

2026 is a year of opportunity—because the odds improve for buyers who plan properly.

Not a “cheap market,” not a “panic market.” More like a stable, normalising market with selective opportunities.

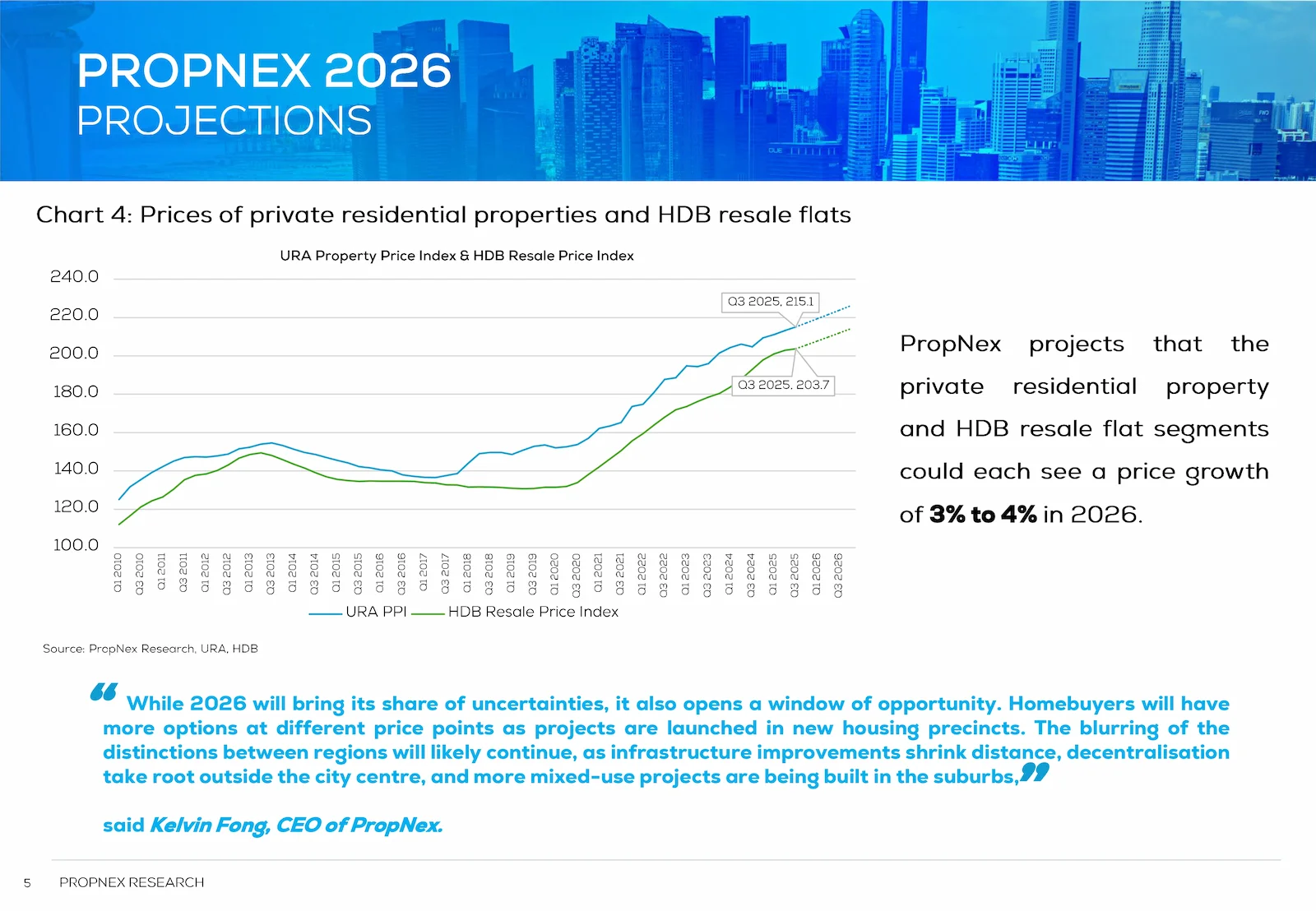

PropNex base case for 2026: both private residential and HDB resale prices projected +3% to +4%. (Source: PropNex 2026 Property Market Outlook Report).

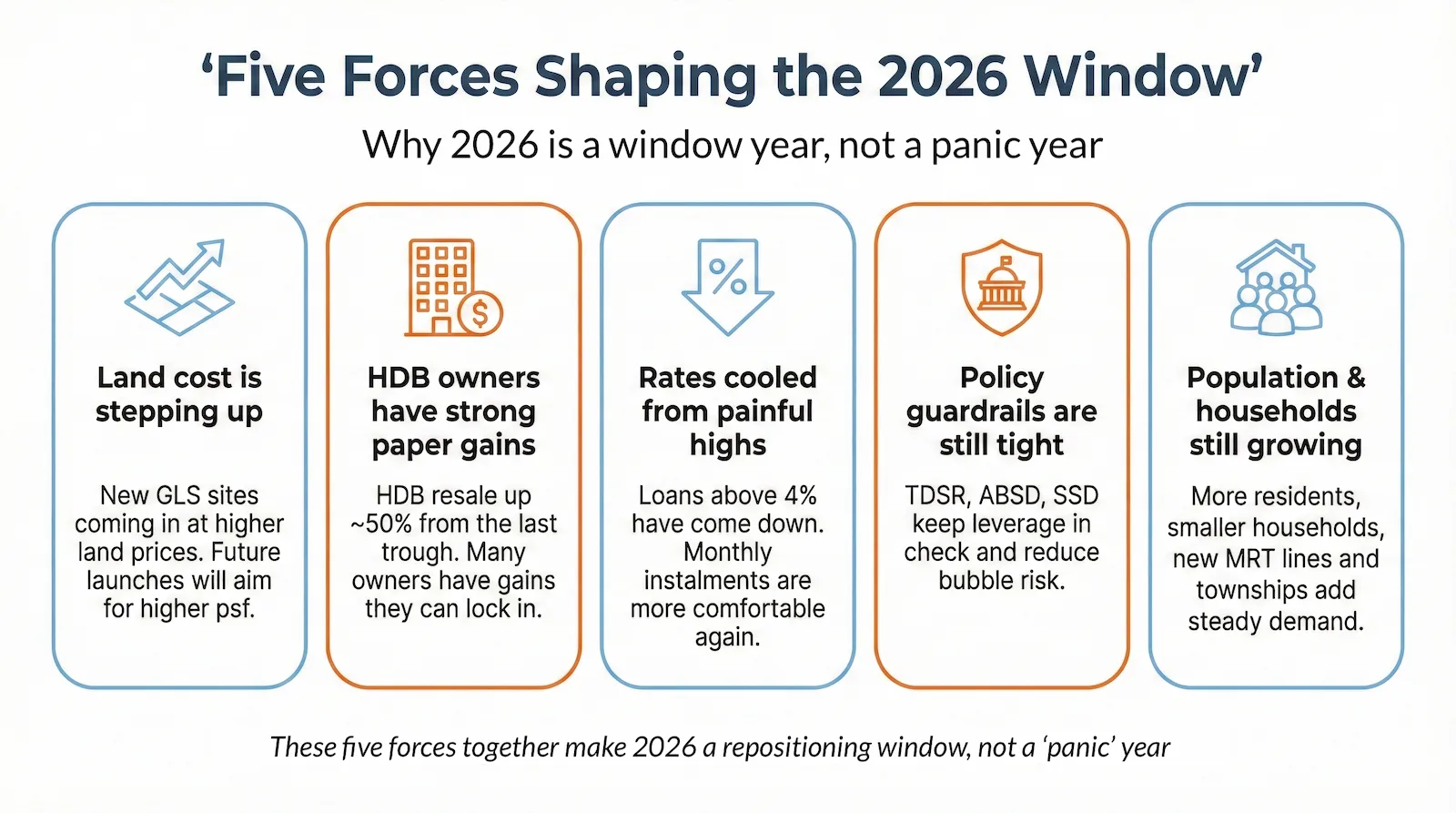

Section 1 summary: the five forces shaping 2026.

Here is exactly how these five macro forces are moving together to create this unique market window:

i. Land cost is stepping up

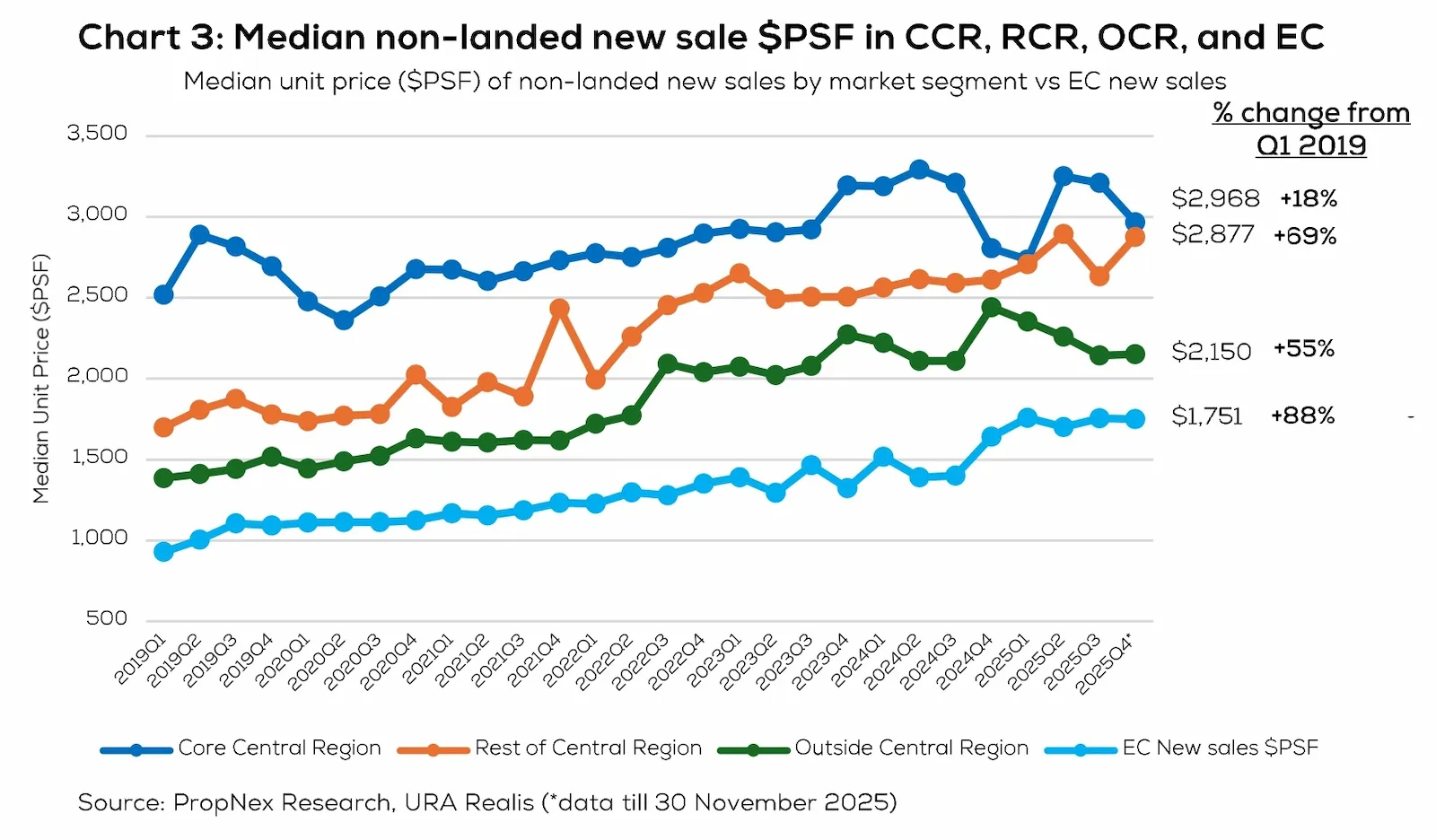

New GLS sites for OCR and RCR are coming in at higher land prices. Future launches anchored on this “new land” will naturally aim for higher psf. Many projects selling today are still based on older, cheaper land — which is why 2026 can be the last leg of the “old pricing” cycle for some segments.

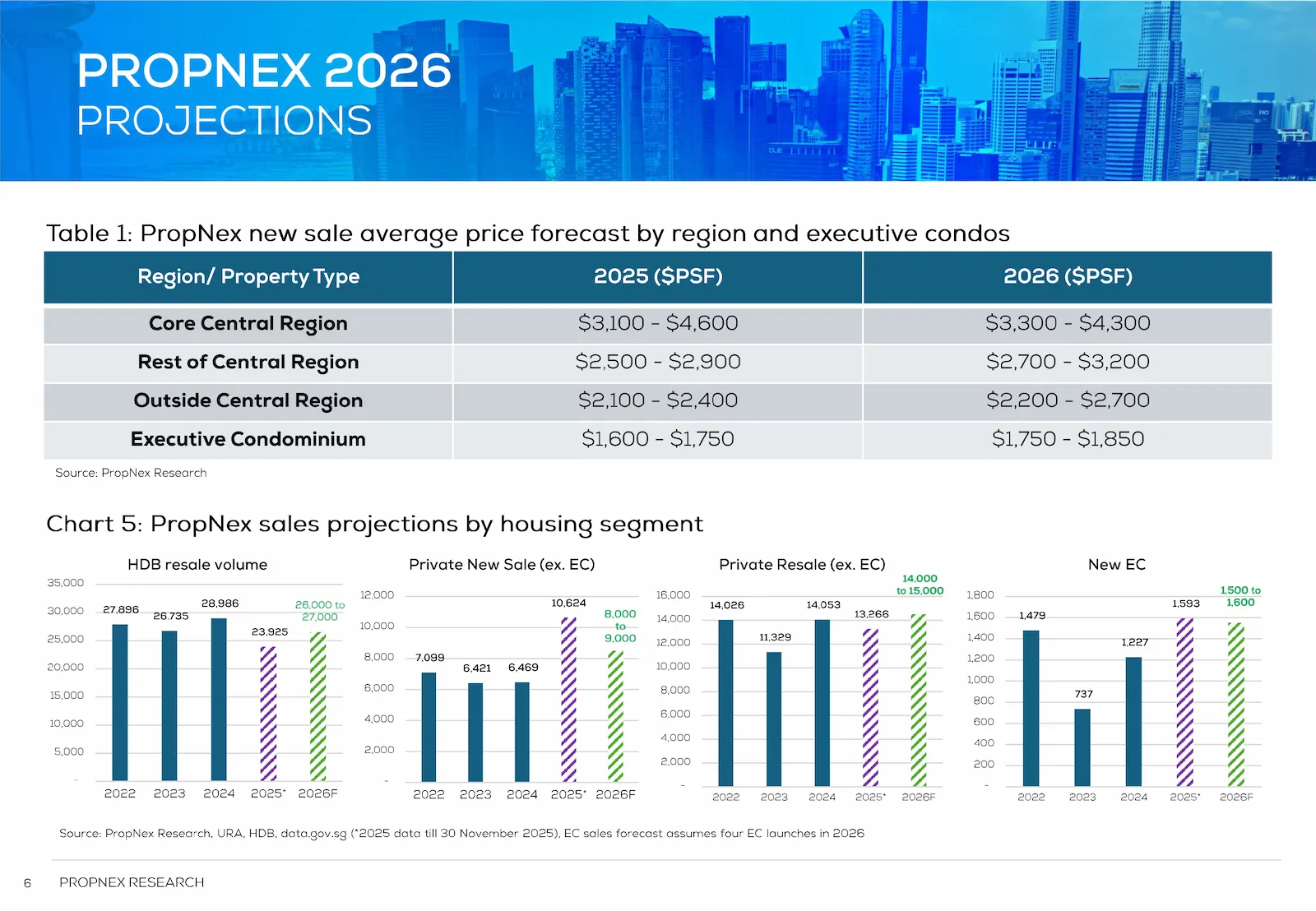

PropNex summarises this reality using illustrative new-launch price bands by region (CCR/RCR/OCR/EC). Think of it as “pricing gravity” — not a framework, but a useful reference for what future launches tend to defend once land costs reset.

CCR ~$3,300–$4,300 psf, RCR ~$2,700–$3,200 psf, OCR ~$2,200–$2,700 psf, EC ~$1,750–$1,850 psf.

- See Table 1 on next page.

PropNex 2026 projections: (1) indicative new-launch price bands by region (CCR/RCR/OCR/EC), and (2) projected sales volumes by housing segment. (Source: PropNex 2026 Property Market Outlook Report.)

ii. HDB owners are sitting on strong paper gains - but timing matters

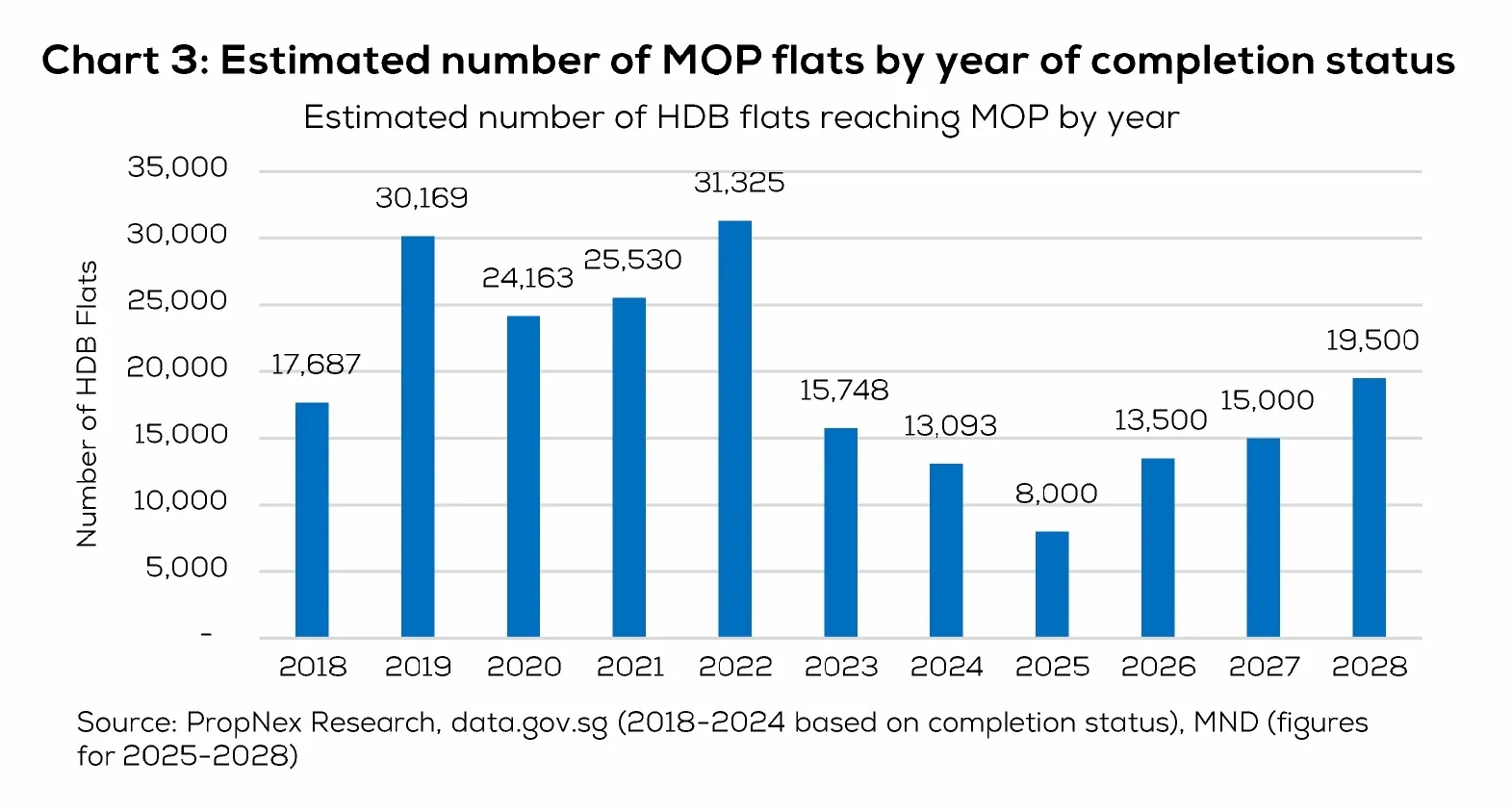

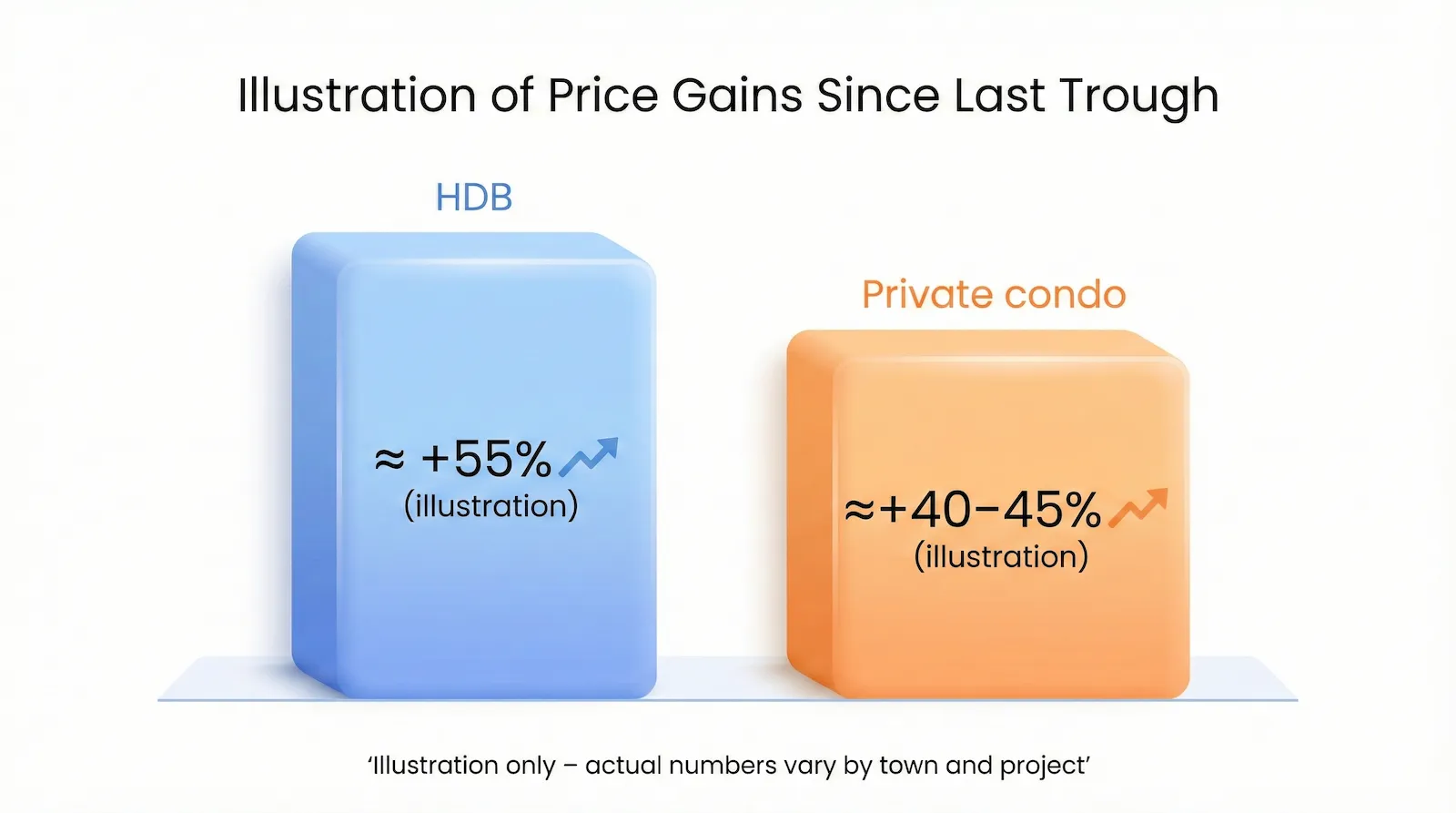

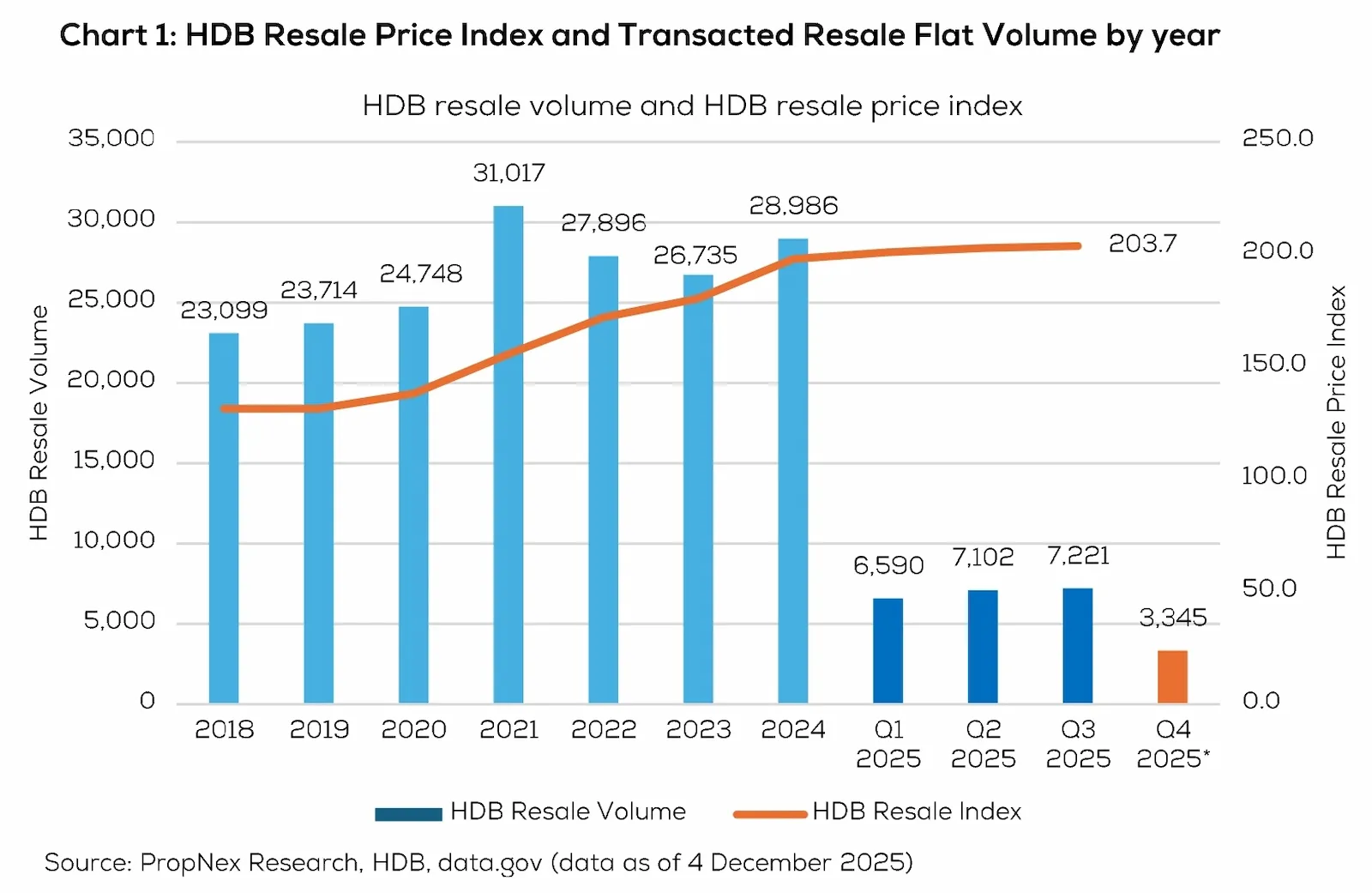

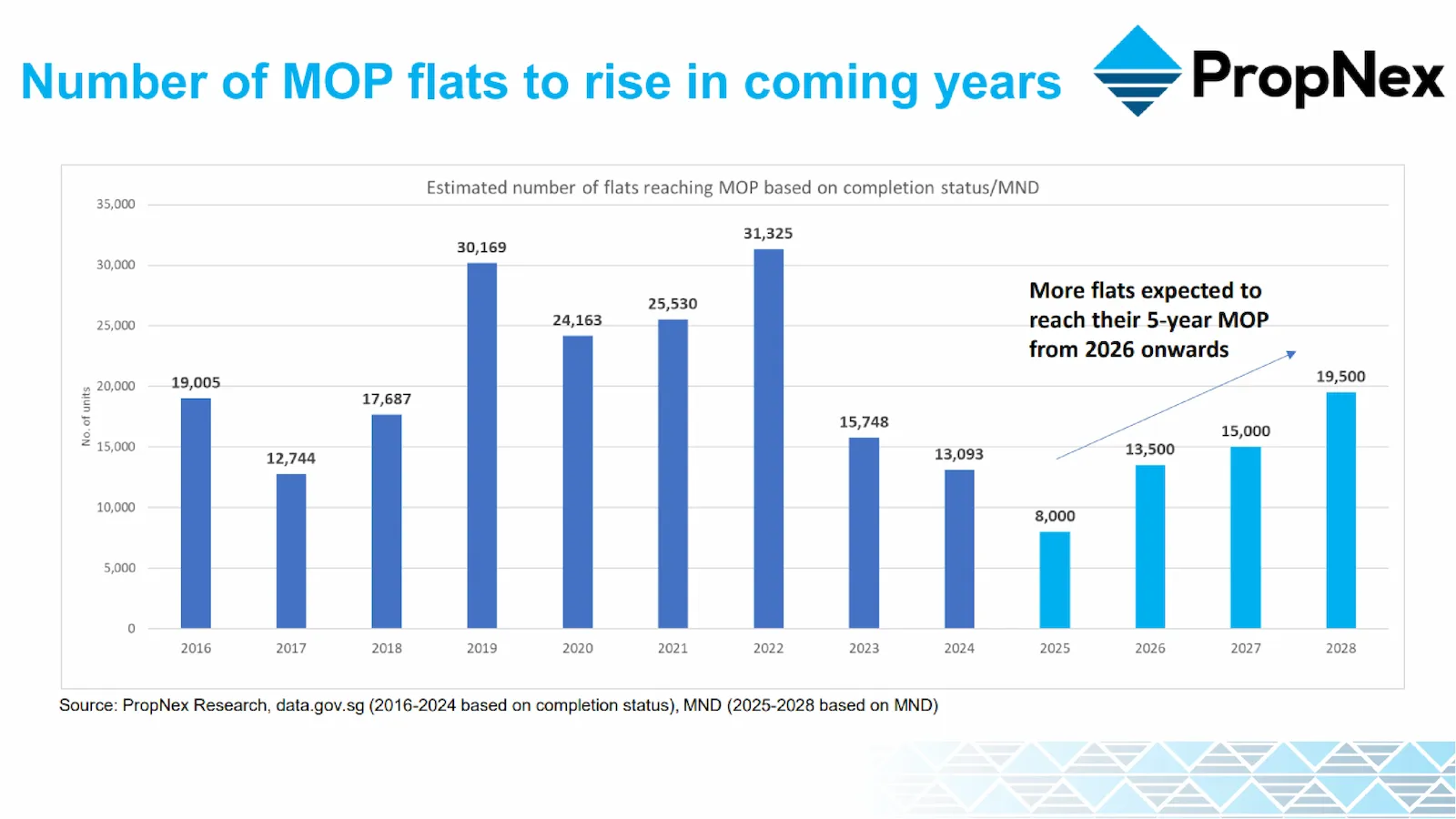

Since the last trough, HDB resale prices have climbed sharply—roughly mid-50% on average. On paper, many owners have already “made money”—but it's not locked in until they sell. At the same time, price growth is already slowing, while a large wave of newer flats will hit MOP from 2026 onwards.

PropNex projects ~13,500 flats reach MOP in 2026, 15,000 in 2027, and 19,500 in 2028 — meaning resale supply normalises and buyers get more choices.

(See Chart 3 below.)

Chart 3 (supports Force ii): MOP supply rises from 2026–2028 → more resale choice, more normal market conditions. (Source: PropNex 2026 Property Market Outlook Report).

iii. Interest rates have cooled from painful highs

Home loan rates that went above 4% are now back to a more comfortable range. For the same loan, monthly instalments can be hundreds or even thousands lower than during the peak—even though we didn't see a big pullback. The monthly “pain” of holding a property is lower… at least for now.

For demand, this matters even more. When instalments come down from 4-plus% to something more comfortable, a few things tend to happen: buyers who were “on the fence” in 2022–2023 suddenly find the math workable again, HDB upgraders feel braver about taking on a condo loan, and some investors who made money in stocks start rotating part of their gains into property. It doesn’t mean a crazy boom, but it does mean a broader base of genuine demand for well-located OCR/RCR projects once people feel that “rates have normalized.”

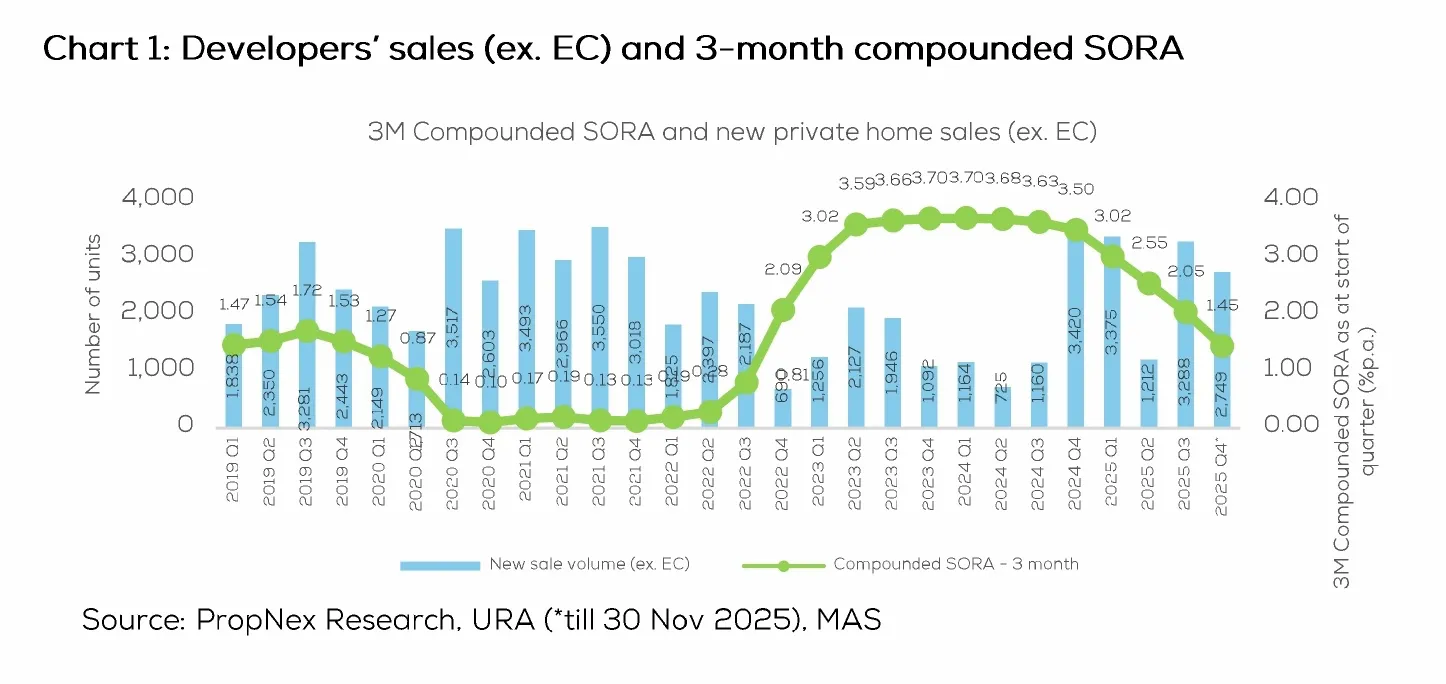

PropNex notes 3-month compounded SORA was ~1.22% p.a. (9 Dec 2025), down from ~3.02% at the start of 2025 — see Chart 1 below. This is why affordability and confidence can return even without prices “falling nicely”.

See Chart 1 below — as SORA eased, new-home sales recovered.

Chart 1 (PropNex): As SORA eased, new-home sales recovered — affordability is a demand trigger. (Source: PropNex 2026 Property Market Outlook Report)

From rate cuts to real-world demand—lower rates can boost stocks, encourage investors to capture value, and eventually send more money back into the property market.

Investor Note (secondary effect): Because ABSD for foreigners is high, many can’t easily buy Singapore residential property directly. Some express Singapore exposure via property-related stocks/REITs instead. When rate relief lifts markets and sentiment improves, a portion of that confidence can spill over into real housing demand (upgraders and investors).

iv. Policy guardrails are still tight

TDSR, ABSD, and SSD don’t stop prices from moving, but they reduce the chance of a crazy bubble and force buyers to think longer term. Investors can’t buy multiple units and flip. That keeps the market more “boring”—and boring is good for families.

(See Section 1.1 (next page) – 2026 Market Setup: Opportunities & Challenges.)

PropNex flags policy risk remains a swing factor (including prospects of further cooling measures), even as recent price gains have been more modest.

v. Population and household demand are still growing

Over the next few years, Singapore is planning for more residents and more households, not fewer:

- Smaller average household size

- More singles, young families and retirees, each needing their own unit

- New MRT lines and amenities coming up around key growth nodes

(See Section 1.1 (next page) – 2026 Market Setup: Opportunities & Challenges.)

Supply can move in cycles, but the long-term demand story is still anchored in real people, not just speculation.

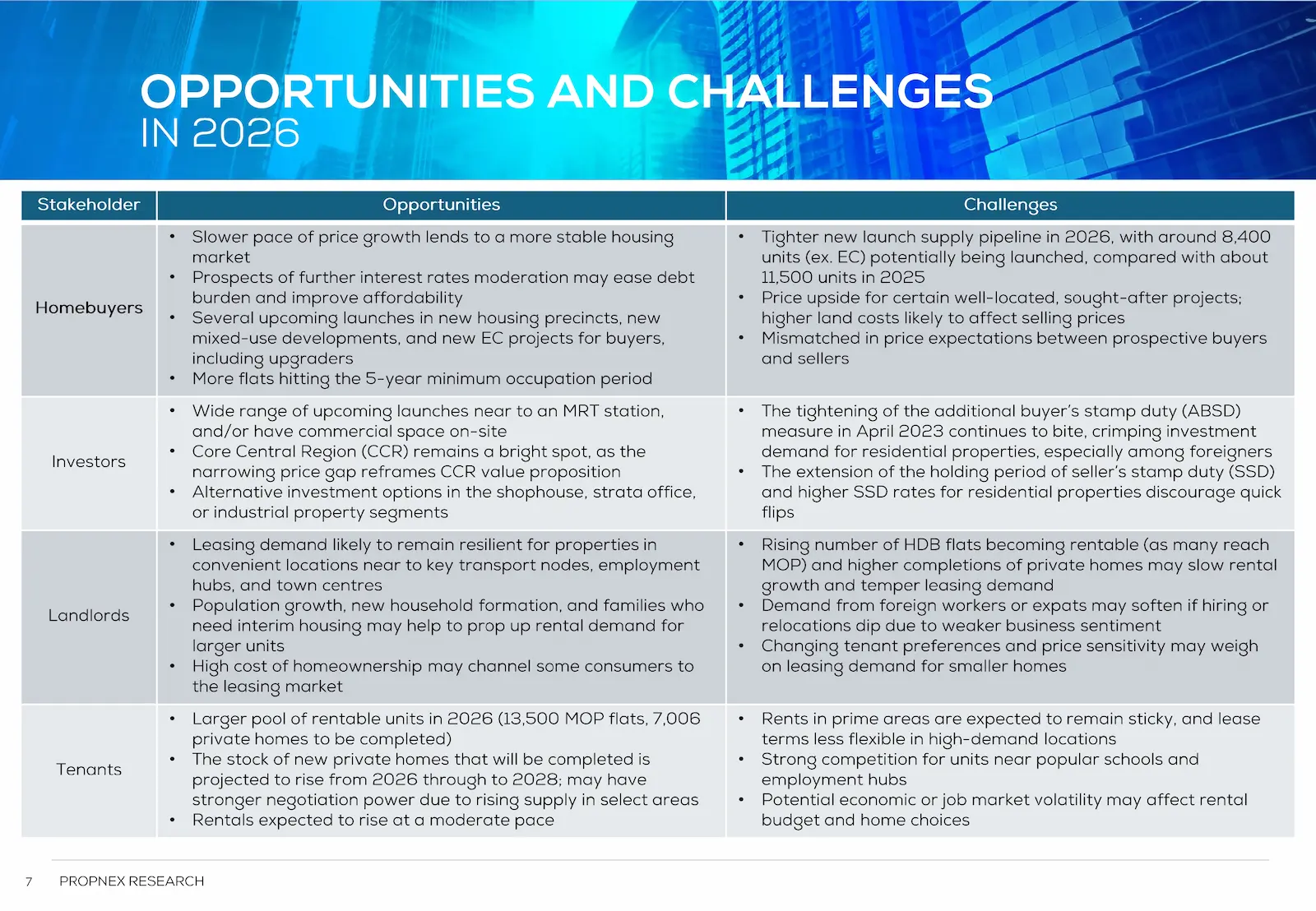

1.1 2026 Market Setup: Opportunities & Challenges

Balanced 2026 view: tailwinds and headwinds can coexist — plan based on your role (homebuyer / upgrader / investor). (Source: PropNex 2026 Property Market Outlook Report).

PropNex’s framing is useful because it keeps 2026 balanced: not hype, not fear. Rates cooling improves affordability and confidence, while supply and pricing remain selective because land costs and pipeline constraints still matter. For buyers, the takeaway is simple: 2026 rewards clarity + planning + holding power more than waiting for a dramatic “cheap market” that may not arrive. Use this guide to match your move to your role — upgrader, first-time condo buyer, or investor — then execute with buffers.

1.2 The HDB “Double Wave”

On top of this, there is what I call the HDB double wave:

- • Wave 1 – Big HDB price gain.

From the last trough to now, HDB resale prices have already climbed a lot (around mid-50% on average). Many owners are sitting on very decent paper gains.

In the last cycle, HDB has outpaced private—but paper gains only matter if you know how to use them.

- • Wave 2 – Upcoming MOP/BTO supply wave.

Between 2026 and 2028, a large batch of newer BTO flats will hit their 5-year MOP and enter the resale market. That’s a lot of competing flats for sale within a relatively short window.

If you're an HDB upgrader, see Section 5.1 for how this second MOP wave can affect your timing and upgrade gap.

Put simply:

- Wave 1 is past price gain.

- Wave 2 is the upcoming supply.

When you put both waves together, the risk for upgraders is this: if you keep waiting for “a bit more” upside on your flat, but the MOP wave slows HDB prices while private condo prices step up on new land cost, your upgrade gap can quietly widen instead of improving.

Separately, future policy tweaks—for example, changes to the 15-month wait-out rule—can also shift HDB demand and supply. But even without that, the double wave of past gains and upcoming MOP supply is already enough reason to plan carefully.

1.3 What This Window Really Means

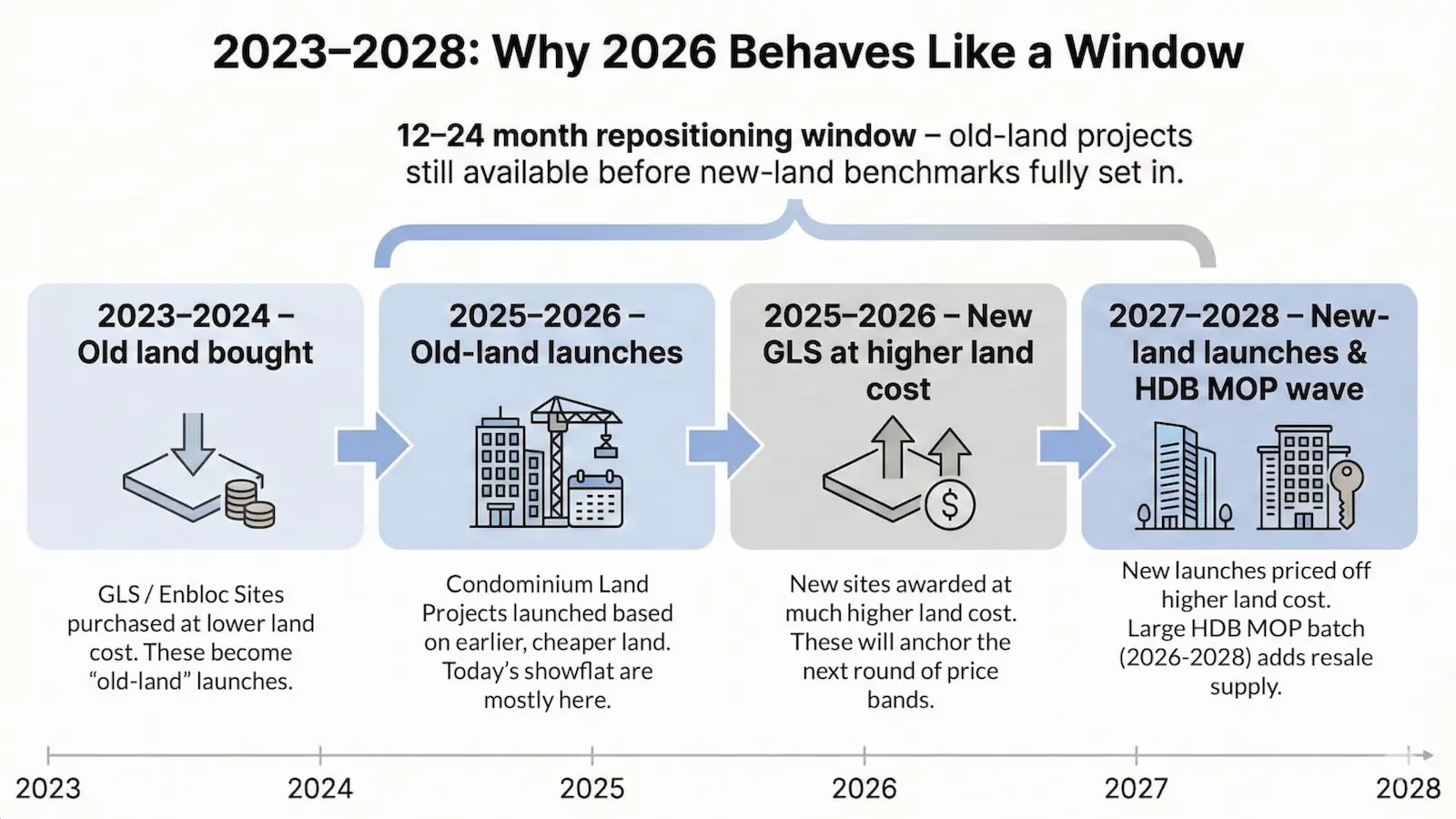

Put together, 2026 is not a “big-discount” year. It's a transition window:

- Old-land projects are still selling in today’s market.

- New-land launches will likely anchor tomorrow’s prices.

- HDB upgraders, condo buyers, and investors have roughly 12–24 months window to reposition before the next step-up becomes the new normal.

From land purchase to launch and HDB MOP—2023 to 2028. 2026 behaves like a window year because old-land launches, new-land GLS, and the HDB MOP wave all overlap within roughly 12–24 months window.

For serious buyers, the bigger risk isn’t “What if I buy at the peak?”

It’s this:

“What if I wait until both HDB and condo prices move against me—and miss this 12–24 month window completely?”

This guide is here to help you answer that question calmly, using your own numbers instead of headlines.

The goal isn’t to be early—it’s to be prepared.

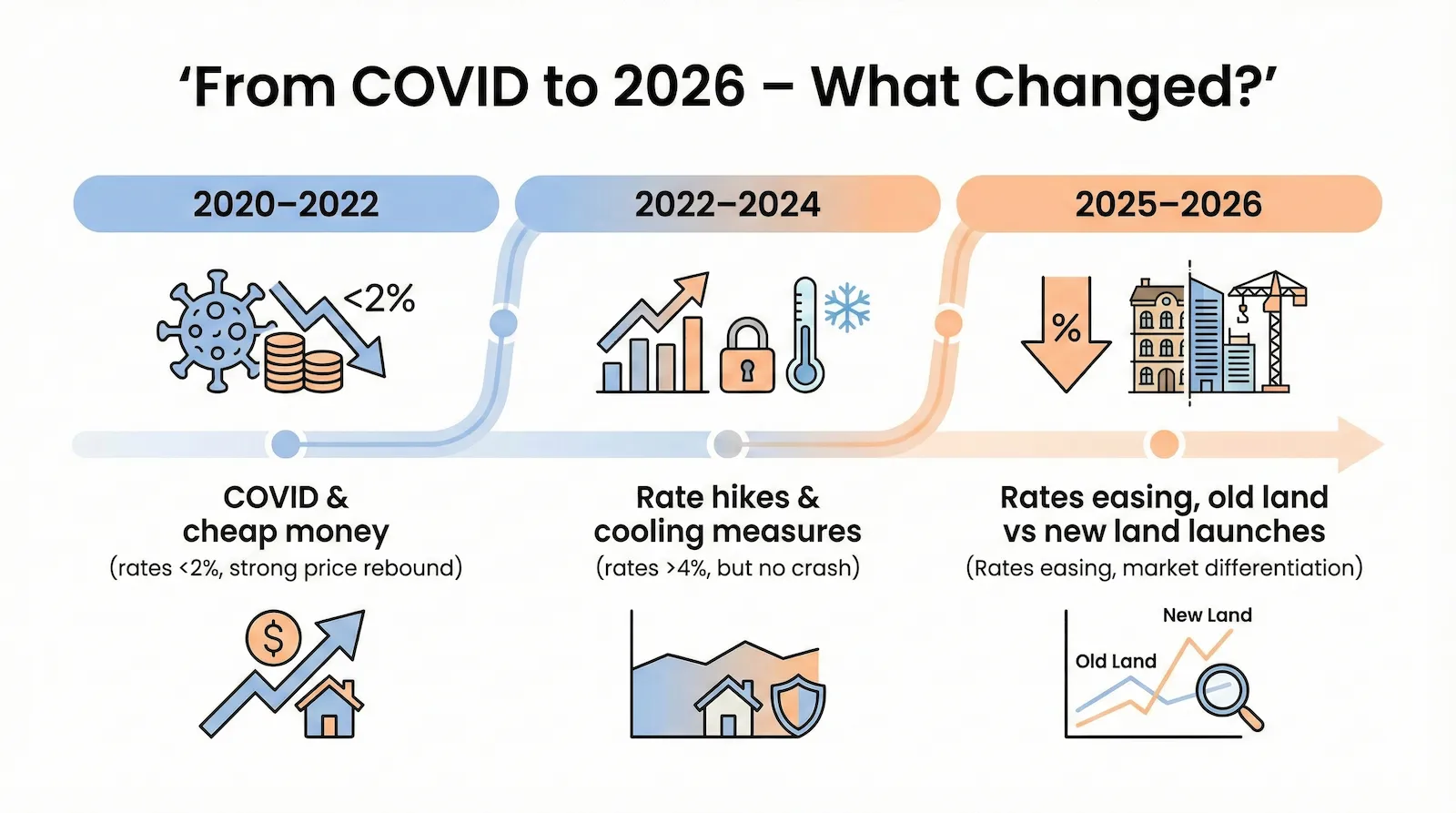

2. From COVID to 2026: What Actually Changed in the Singapore Property Market?

Instead of arguing about whether "property is expensive," let's zoom out a bit.

2.1 2020–2022: COVID, Cheap Money, Surprises

During COVID:

- Interest rates were below 2% for a long stretch.

- Construction delays and manpower issues reduced near-term supply.

- Many households realized their current home was too small, too far, or too inconvenient when everyone was working and studying from home.

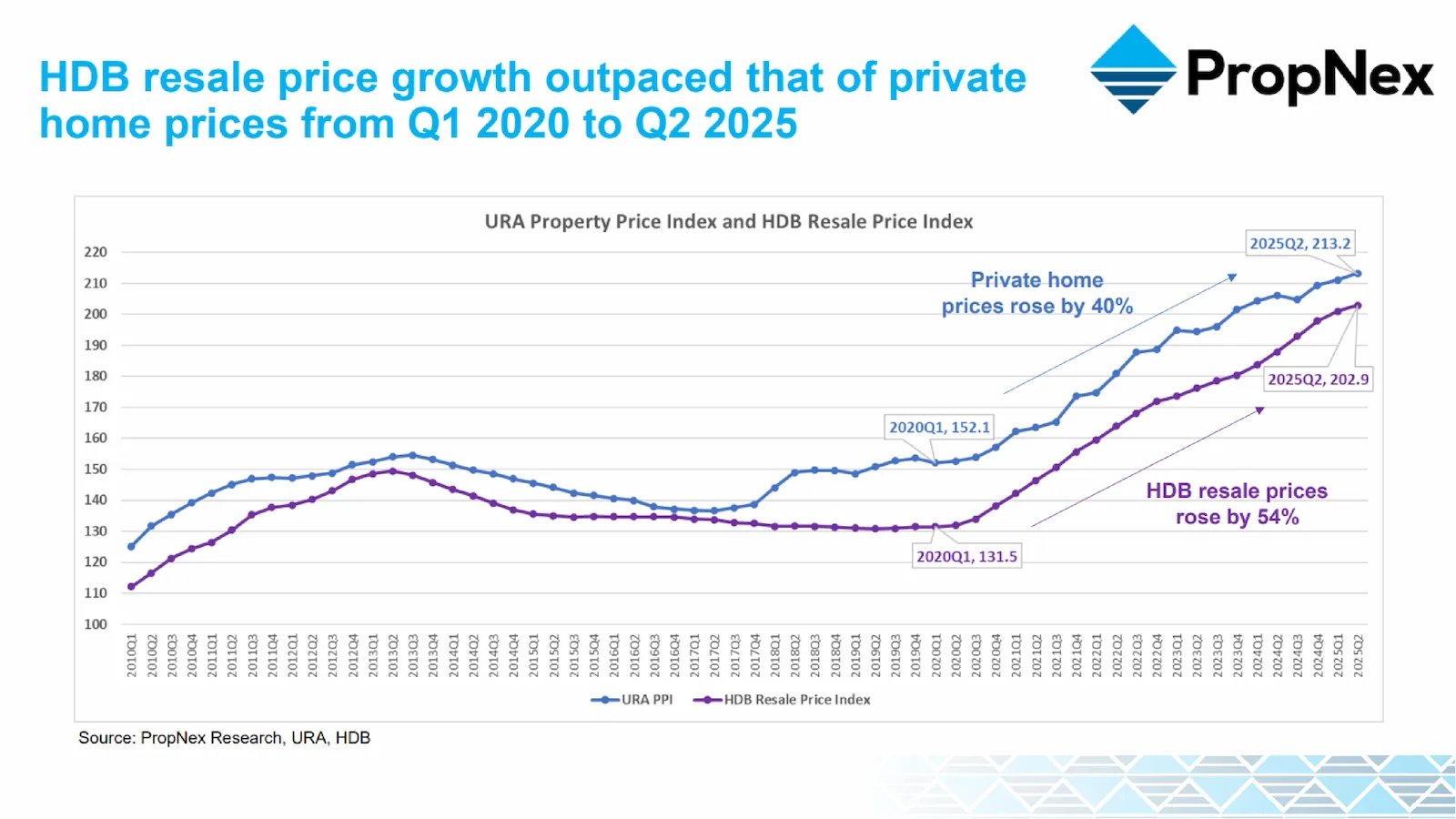

Result: both HDB and private prices climbed strongly off the 2020 low. HDB actually rose faster than private from 2020 to mid-2025.

From 2020 to 2025, HDB resale prices rose faster than private—many owners are sitting on strong paper gains.

2.2 2022–2024: Rate Hikes, Cooling Measures, But No Crash

When global inflation spiked, interest rates shot up:

- Floating and fixed rates moved above 4%.

- Monthly instalments suddenly felt very heavy, especially for highly leveraged buyers.

- The government introduced more cooling measures to prevent runaway prices.

Yet prices did not crash:

- There wasn't a flood of forced selling because TDSR and prudence were already in place.

- Genuine demand—upgraders, first-timers, families—was still strong.

- Supply was still relatively tight, especially in mass-market OCR and good RCR projects.

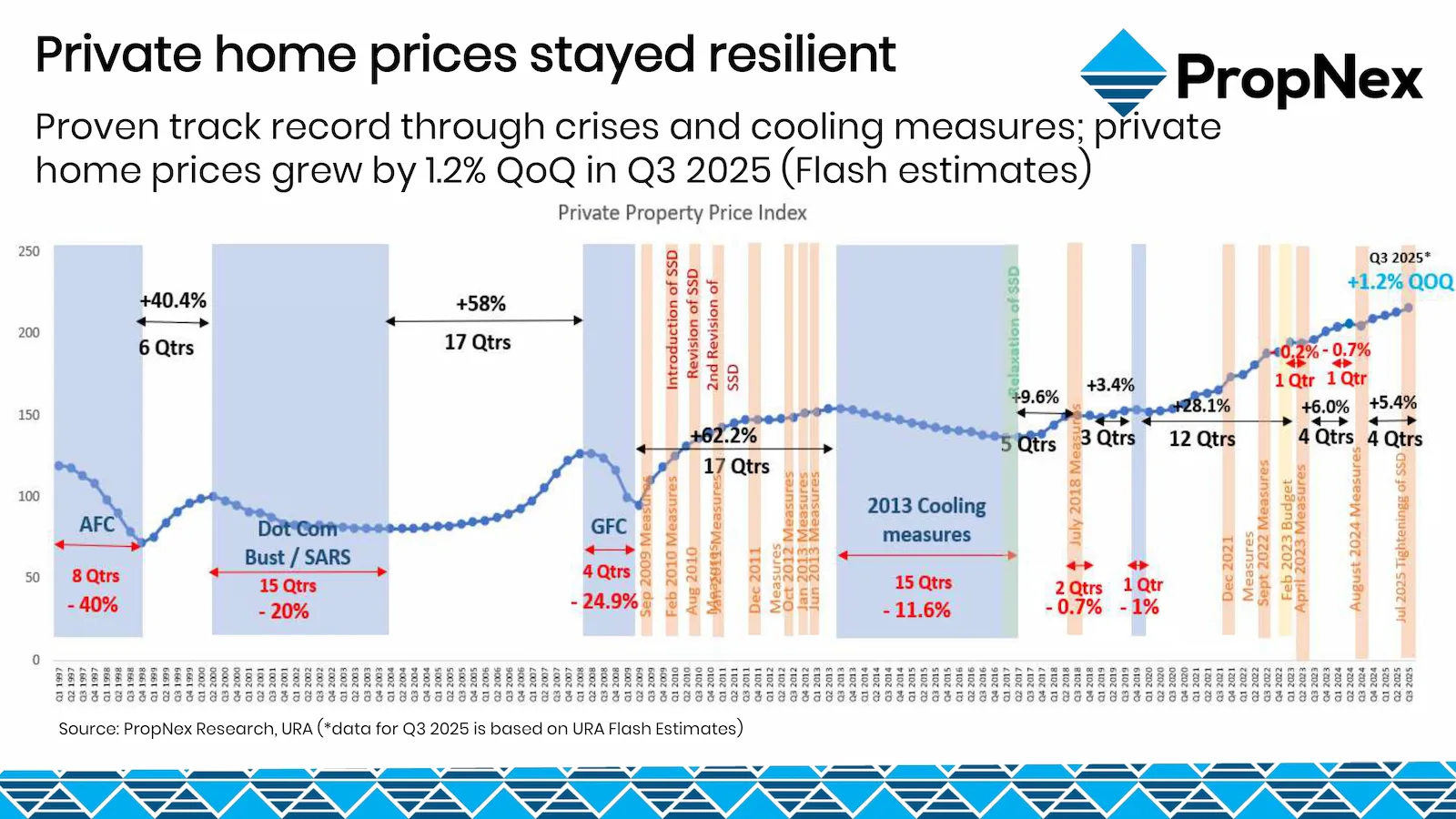

If you look at the long-term private home price index, you'll see the same story. Through AFC, SARS, GFC, the big cooling measures, and even COVID, prices corrected but didn't collapse the way many people feared. The market tends to pause, digest the bad news and new rules, then find a new level—not reset back to 2003 or 2009 prices. The same picture holds for 99-year leasehold condos specifically — what 30 years of leasehold resale prices show is that 99-year stock has followed the same correct-digest-recover pattern, not the steady decay many buyers assume.

Private home prices stayed resilient across crises and multiple cooling measures (URA PPI, PropNex Research; Q3 2025 flash estimate +1.2% QoQ).

Key takeaway: Even through major crises and multiple cooling measures, Singapore private home prices tended to correct, digest, and recover — not "reset" back to old-era prices. That's why 2026 decisions should be based on affordability + holding power, not crash expectations.

2.3 2025–2026: Rates Easing, "Old Land" vs "New Land"

Now, as we head into 2026:

- Home loan rates have started to ease off from the 4%+ peak.

- Developers are still selling projects based on older, cheaper GLS land... but recent GLS bids for OCR/RCR show much higher land cost.

- The pipeline of future launches (especially for OCR family projects) is based increasingly on this new land cost.

This is why we say 2026 is a pricing crossover zone:

- Some launches and resales are still anchored to yesterday's land cost.

- The next wave of launches will have to test tomorrow's price bands.

If you're an upgrader or investor, this is the window to ask:

"Do I want to reposition while some 'old land' options still exist—or do I want to wait until everything is 'new land' and re-decide then?"

Property didn't move in a straight line—but there was no 20–30% crash either.

2.4 Demand Drivers – Wealth, Aspirations & Population

So far we've looked at prices, policies, and interest rates. Behind all that, three long-term demand drivers keep showing up in the data:

Stronger household wealth, rising private-housing aspirations, and steady population growth all help to support demand for sensible private homes over time.

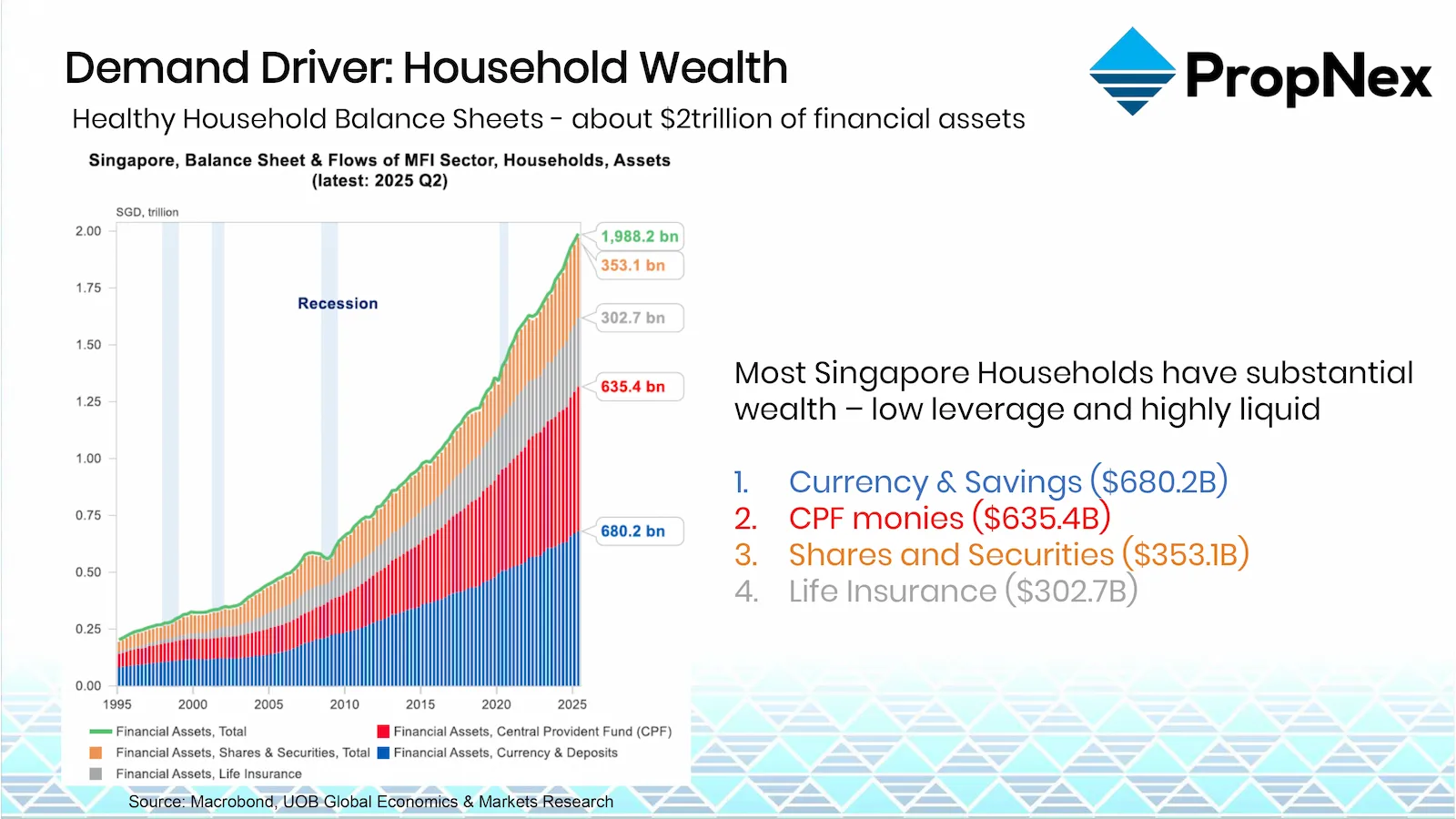

A. Healthy household balance sheets

Over the last 20–25 years, Singapore household wealth has grown steadily. Today, households collectively hold around $2 trillion in financial assets—spread across bank savings, CPF, shares, and life insurance.

Most families are not over-geared. Instead, a lot of wealth is sitting in cash, CPF and liquid investments. When the time feels right, some of this can (and does) rotate into property—whether it's upgrading from HDB, buying a second property, or helping children with their first home.

Singapore households today hold about $2 trillion in financial assets—giving many families the capacity to upgrade when the math works.

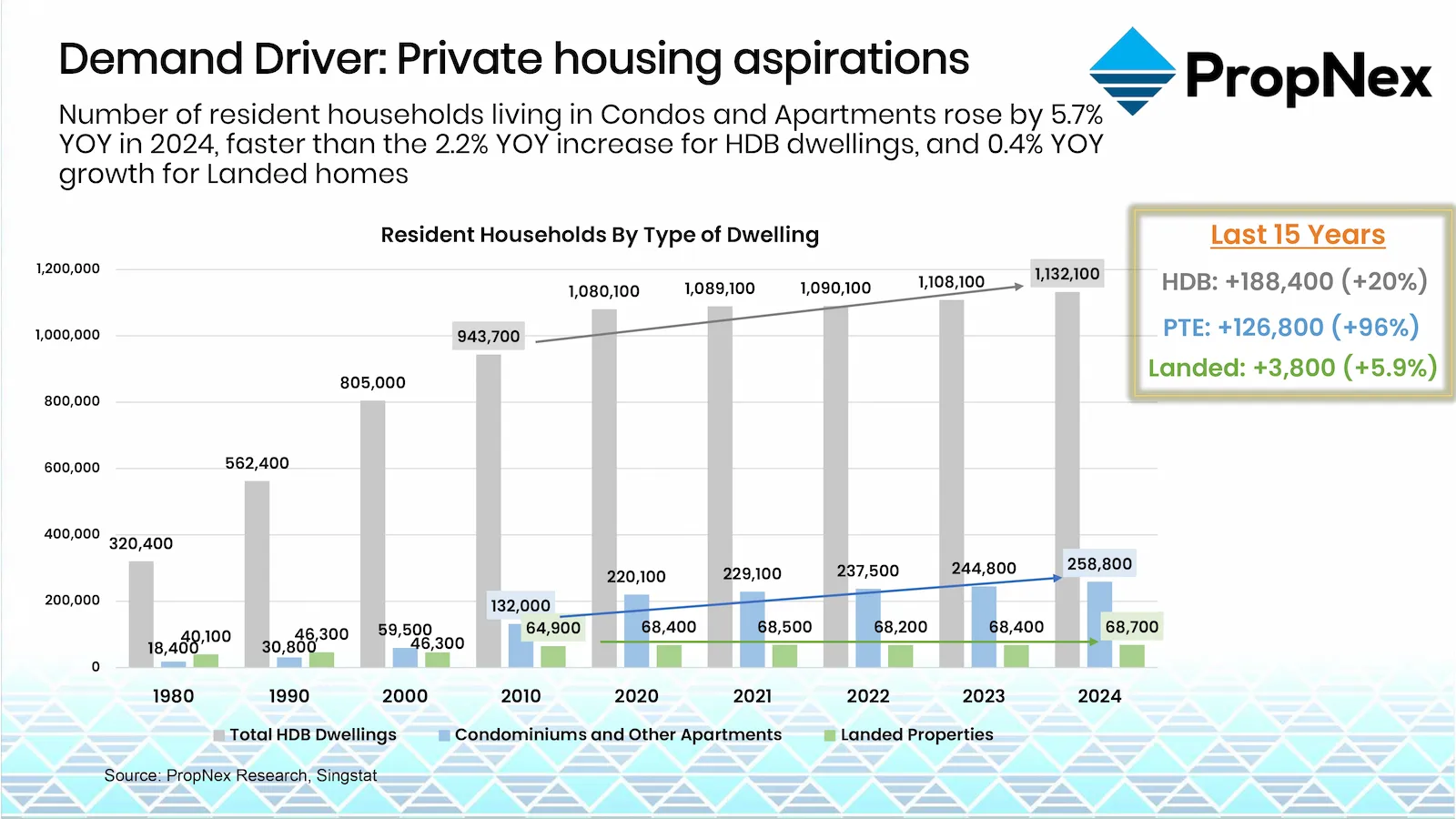

B. Rising private-housing aspirations

Data also shows a clear shift in where people want to live.

In the last 15 years, the number of households staying in condos and apartments has almost doubled, growing faster than HDB and much faster than landed homes. More young families, singles and retirees are choosing private condos for facilities, security and location convenience.

Put simply: private housing is no longer just for a small group of "rich" buyers. It has become a mainstream aspiration for many working households.

Private-home households have almost doubled over the last 15 years—showing a clear, long-term shift towards condo living.

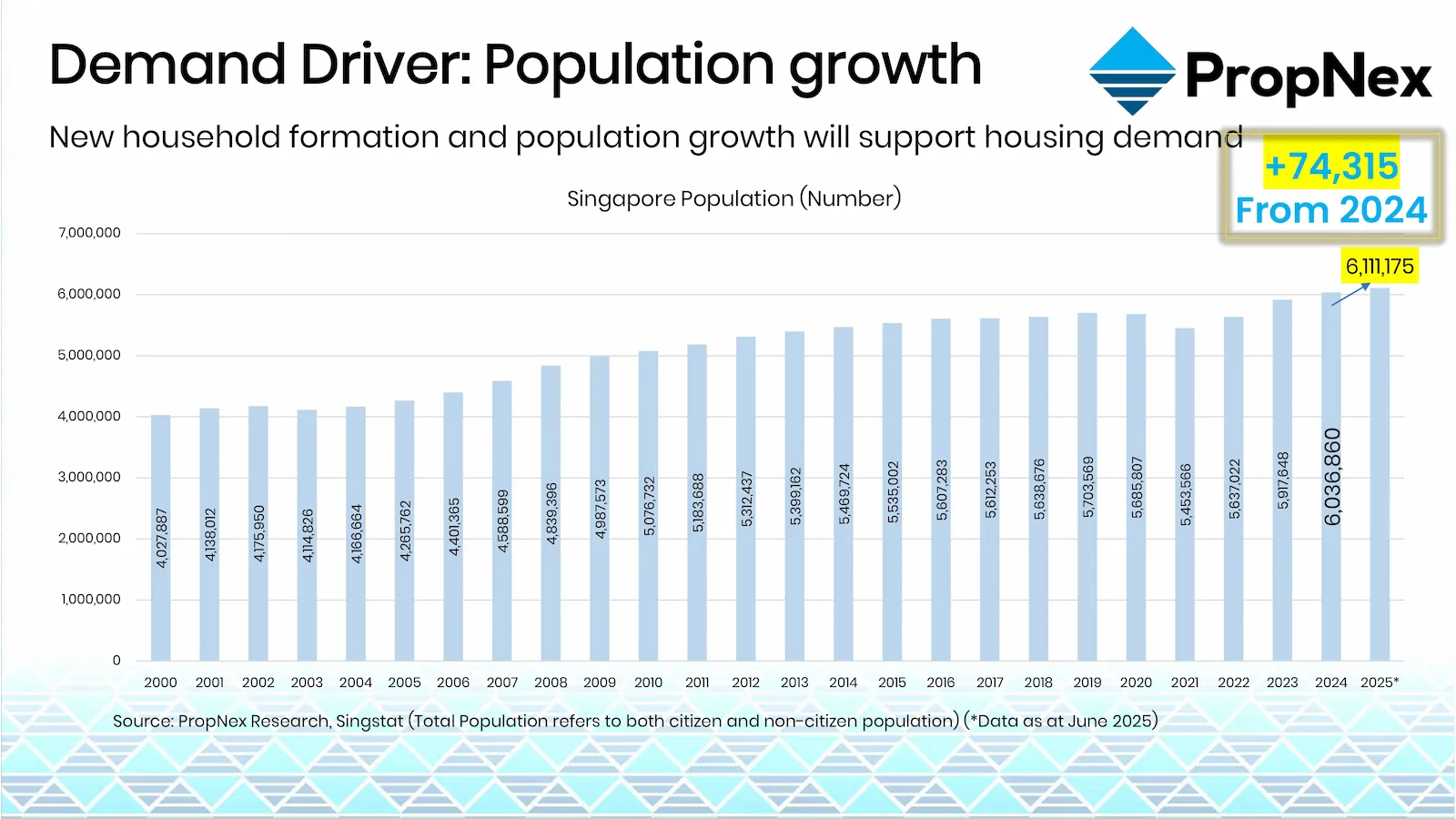

C. Population growth & new household formation

On top of this, Singapore's population and number of households have continued to rise.

Population and household numbers are still trending up—more people and smaller households mean more homes are needed over time.

Even when overall growth is modest, new households keep forming:

- Children moving out and forming their own families

- Singles choosing to live independently

- Foreign professionals and PRs making Singapore their long-term base

Every new household needs a place to stay—HDB, condo, or landed. Over time, this steady increase in households supports demand for both HDB and private homes.

Taken together, these trends suggest that:

- There is real, underlying demand for homes—backed by household wealth, not just speculation.

- The shift towards private housing is structural, not a short-term fad.

- As long as jobs remain stable and Singapore continues to attract talent, demand for livable, well-located private homes is likely to stay resilient.

This doesn't mean prices only go one way or that every condo is a good buy. But it explains why, even after crises and cooling measures, the private property market has remained surprisingly steady over the long term.

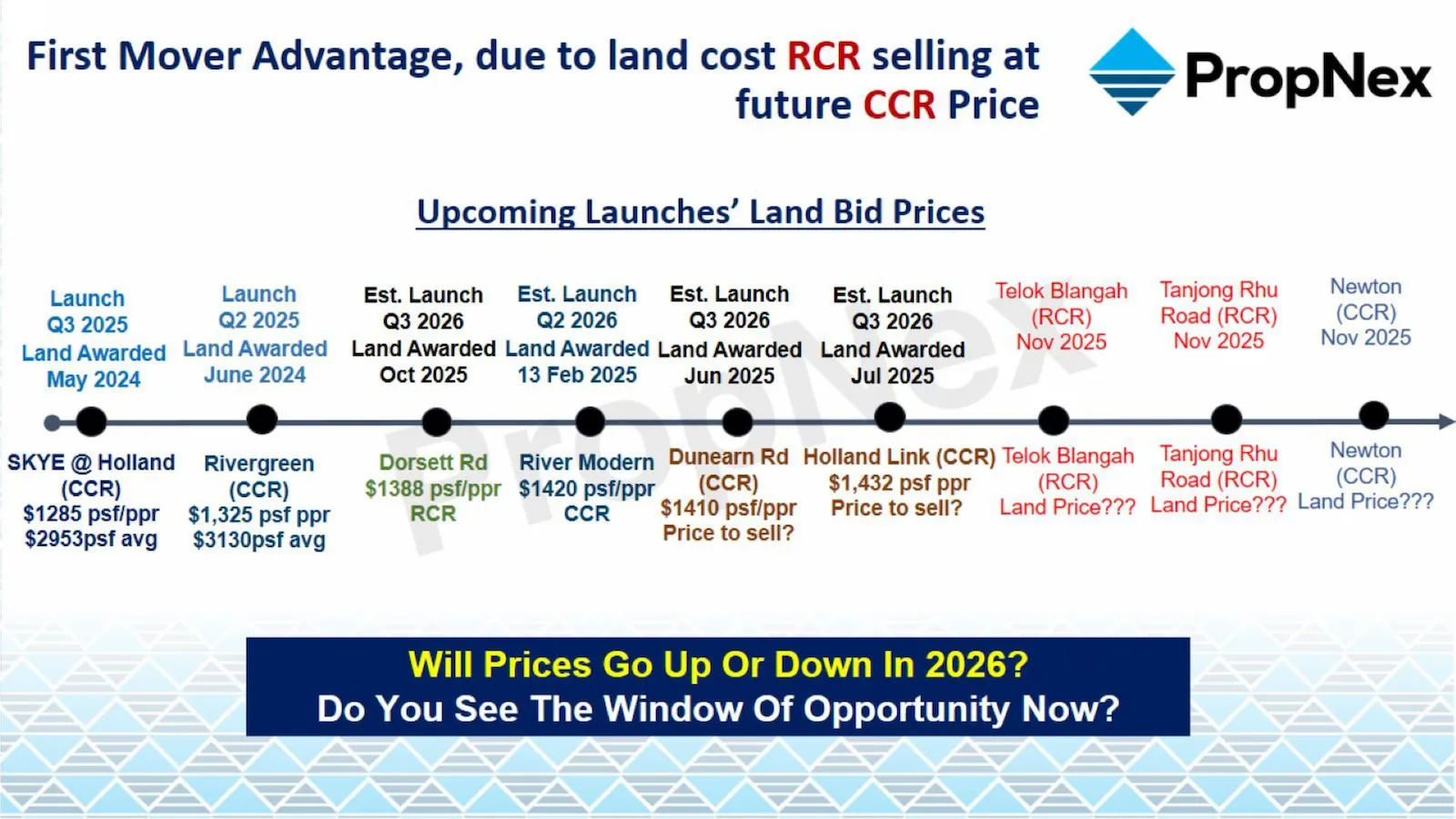

3. New Launch Condo Prices: The "Old Land vs. New Land" Reset

Showflat pricing is not arbitrary; it is a mathematical output of developer land acquisition costs from 12 to 36 months prior. This section decodes the singapore property market outlook 2026 by explaining how the 'old land vs. new land' crossover window mathematically shapes launch prices. A Calculated Entry Strategy requires acting before 'new land' pricing becomes the permanent market floor.

New-launch prices are strictly anchored by four data points:

- Historical GLS land acquisition costs (older vs. newer sites).

- Recent GLS benchmarks setting new minimum launch thresholds.

- The upward shift of land cost bands across CCR, RCR, and OCR.

- The depletion of unsold inventory eliminating developer discount pressure.

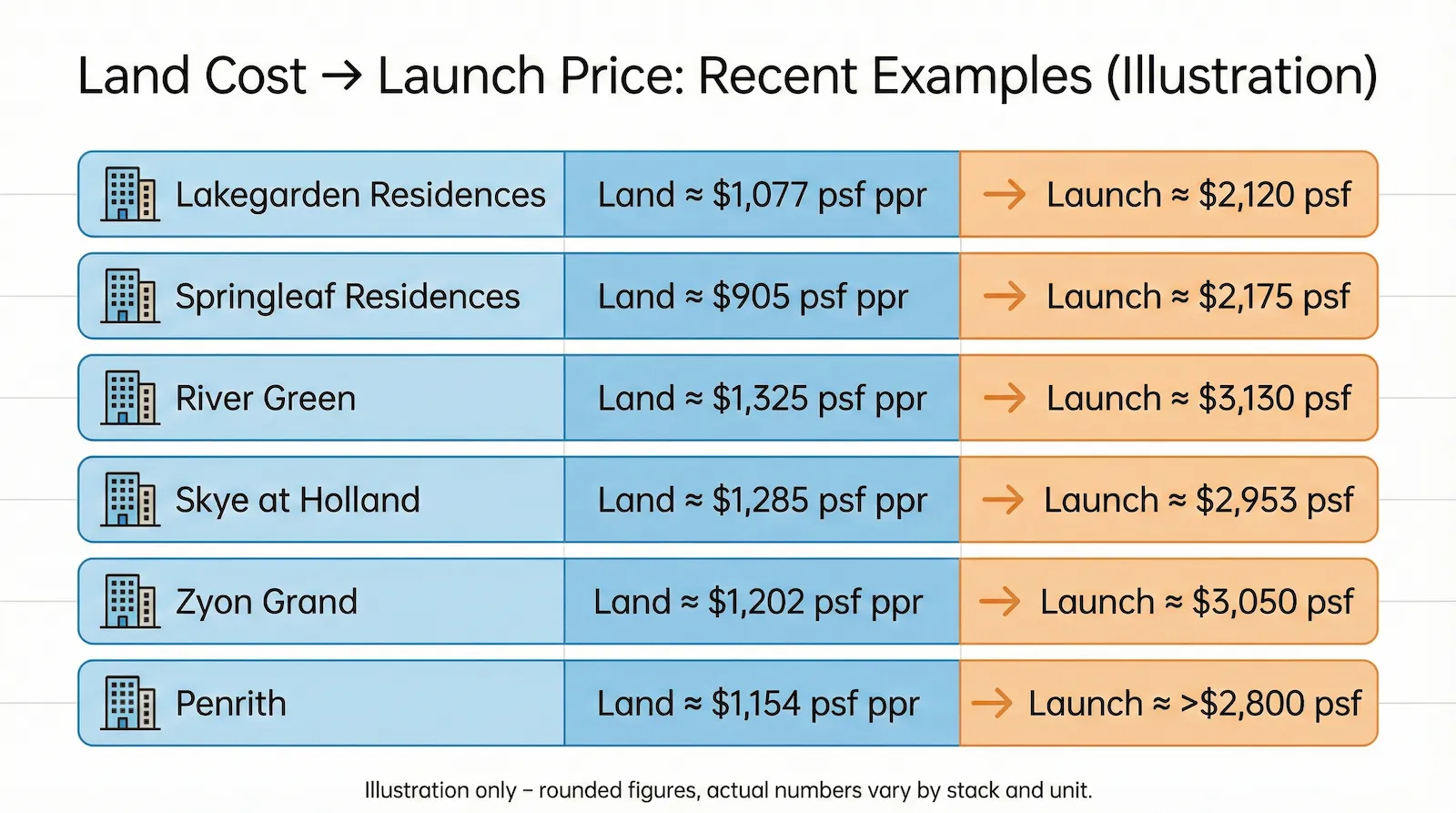

3.1 Real Examples: Land Cost → Launch Price

Here are some recent projects to make the link clearer.

(Figures are rounded and for illustration—exact numbers vary by stack and unit.)

| Project | Land Purchase Date | Land Cost (≈ psf ppr) | Launch Date | Avg Launch Price (≈ psf) |

|---|---|---|---|---|

| Lakegarden Residences | May 2022 | ~$1,077 | Aug 2023 | ~ $2,120 |

| Springleaf Residences | Apr 2024 | ~$905 | Aug 2025 | ~ $2,175 |

| River Green | Jun 2024 | ~$1,325 | Jul 2025 | ~ $3,130 |

| Skye at Holland | May 2024 | ~$1,285 | Oct 2025 | ~ $2,953 |

| Zyon Grand | Apr 2024 | ~$1,202 | Oct 2025 | ~ $3,050 |

| Penrith | Aug 2024 | ~$1,154 | Oct 2025 | > $2,800 |

Even without a detailed cost breakdown, a few things stand out:

- When land is around $900–1,100 psf ppr (Lakegarden / Springleaf), average launch prices tend to sit roughly in the $2,1xx–2,2xx psf range.

- When land steps up to around $1,200–1,300+ psf ppr (River Green / Skye / Zyon / Penrith), launch prices move closer to or above $3,000 psf in stronger locations.

The exact multiplier will differ by project. The main point is higher land cost becomes the new "floor" for future launches in that segment.

Plain-English takeaway:

What you see at the showflat today is not random. It's anchored to what the developer paid for land 1–3 years ago.

3.2 New Land, New Benchmarks—2026 Sites Coming Up

Now look at the next wave of land purchases, which will drive 2026 launches:

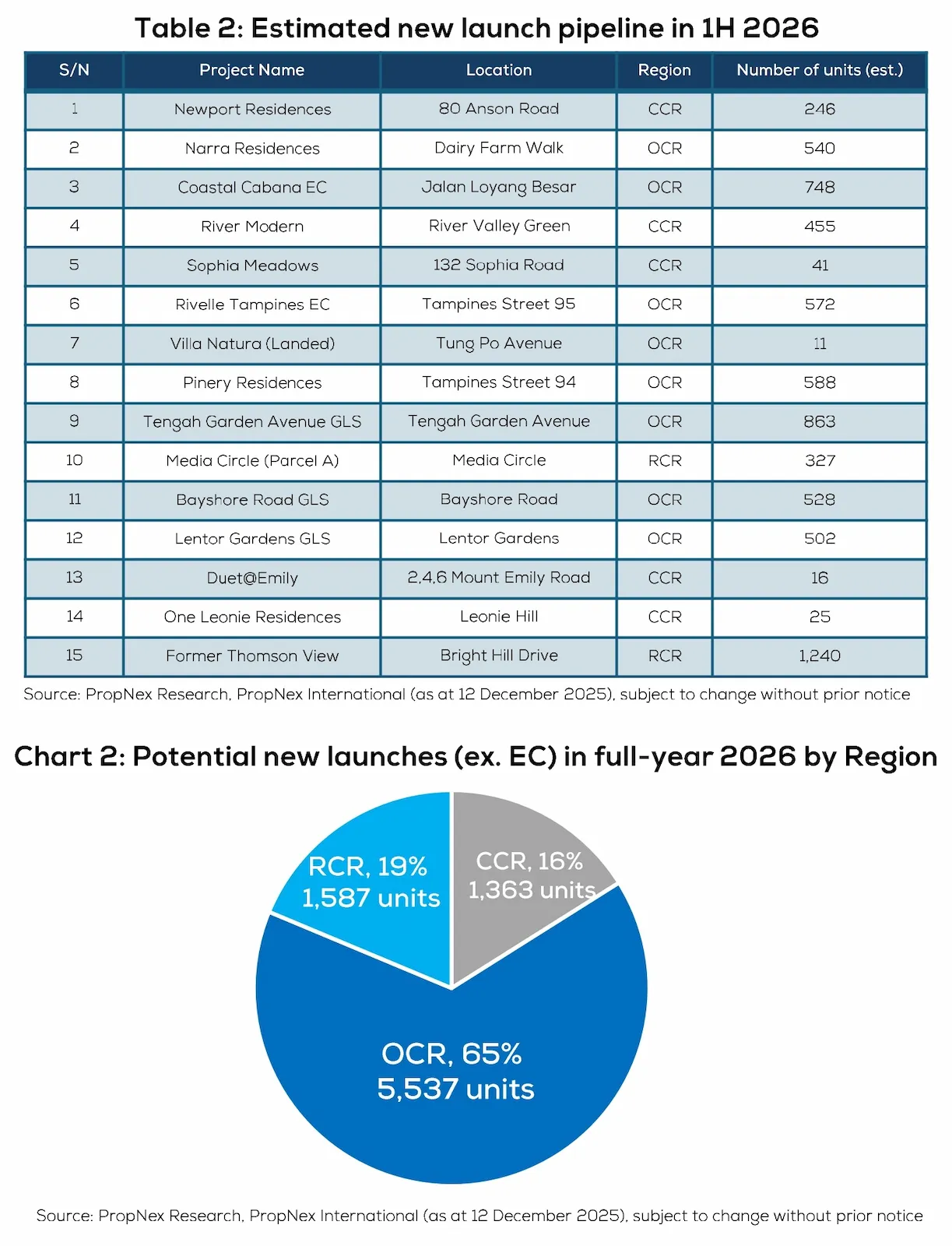

2026 Launch Pipeline. (Source: PropNex 2026 Property Market Outlook Report).

PropNex estimates the 2026 new launch pipeline (ex-EC) at roughly ~8,400 units, and notes that a large share is OCR-led. This matters for our "old land vs new land" story: mass-market demand is still real, but buyers will become more price-sensitive and selective. It also explains why the next round of launches anchored to newer land costs can reset benchmarks even if the market doesn't "run hot".

We're not trying to predict an exact psf for each of these.

But we can ask some sensible questions.

If:

Skye / River Green / Zyon are already launching near or above $3,000 psf on land in the $1,2xx–1,3xx psf ppr range…

Then for:

- Bayshore at $1,388 psf ppr, and

- Newton at $1,820 psf ppr,

is it realistic to expect launch prices to be

- Lower than today's top CCR/RCR launches? or

- More likely to set a new, higher band that becomes the "new normal" for those locations?

Higher land cost today becomes the starting point for tomorrow's launch prices.

This is where the "old land vs. new land" window becomes very real:

- Many projects selling today are still based on pre-2024 / early-2024 land prices.

- Many projects launching from 2026 onwards are based on much higher land costs—especially in RCR and OCR corridors that used to be much cheaper than CCR.

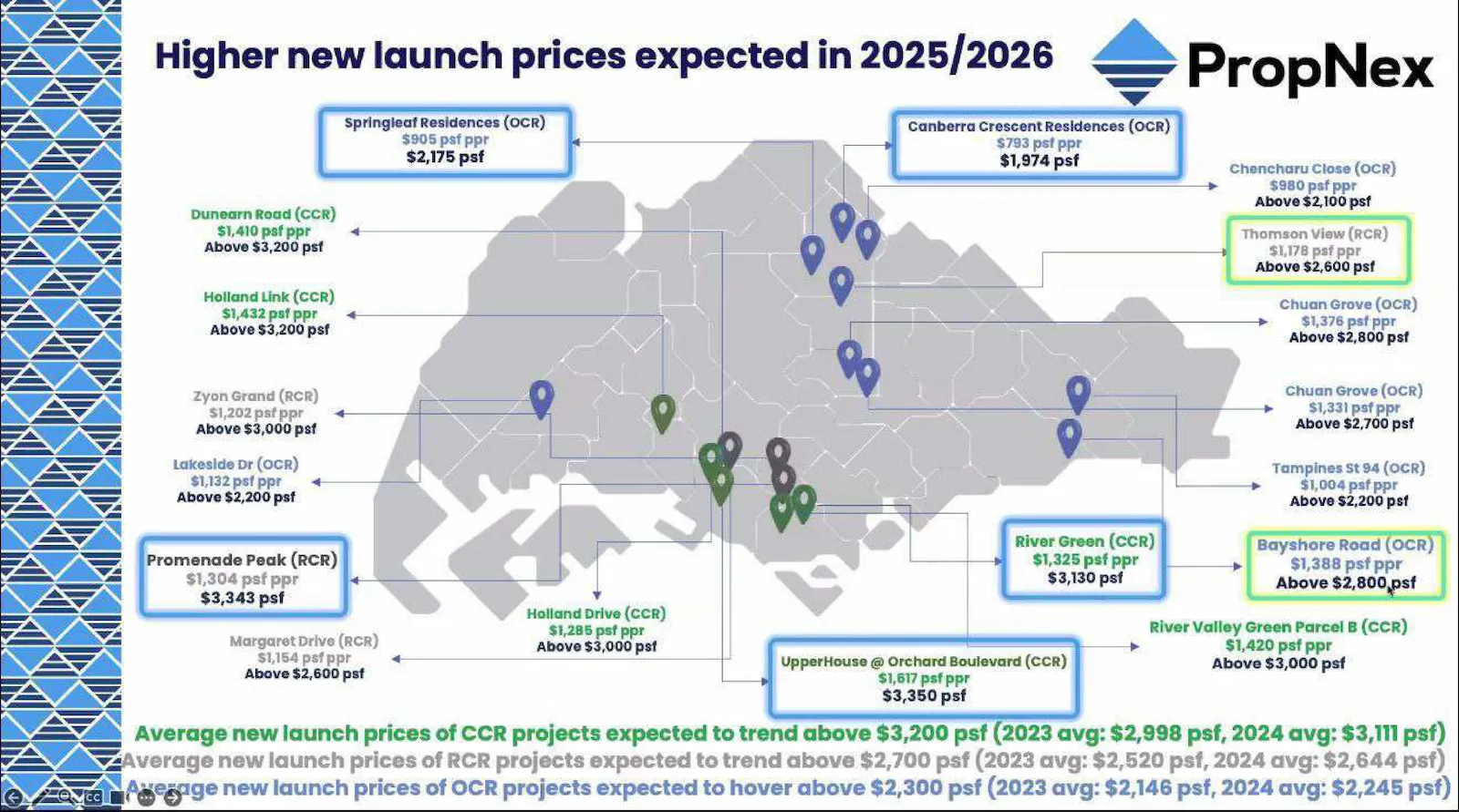

Here are a few recent 2025 GLS sites and their land costs. You can roughly guess which 2026 launch price band each one might sit in.

| Project | Land Purchase Date | Land Cost (psf ppr) | Est. Launch Price Band? (2026) |

|---|---|---|---|

| Thomson View | Nov 2025 | $1,178 | Make A Guess? |

| Chuan Grove A | Jul 2025 | $1,376 | |

| Chuan Grove B | Sep 2025 | $1,331 | |

| Bayshore | Mar 2025 | $1,388 | |

| Lakeside Drive | Jun 2025 | $1,132 | |

| River Modern | Feb 2025 | $1,420 | |

| Newton | Nov 2025 | $1,820 |

Illustration only—land cost based on public data; actual launch prices will depend on design, unit mix, timing, and sentiment.

A live 2026 confirmation of this old-land vs new-land arithmetic: Hudson Place Residences sits on a site secured in March 2025 at roughly $1,036 psf ppr — and launched in May 2026 at an average $2,458 psf, deliberately calibrated below the $2,500 psf quantum ceiling. That is exactly the land-cost-to-launch-price math this section is mapping, playing out in real time.

The Bayshore $1,388 psf ppr row in the table above has its own 2026 confirmation: Vela Bay at Bayshore Walk is the 515-unit SingHaiyi launch built on that exact GLS site, with indicative pricing between $2,800 and $3,000 psf. Same arithmetic, second live read — the 2025 land-cost reset translating into the 2026 launch price band the table is implicitly asking you to estimate.

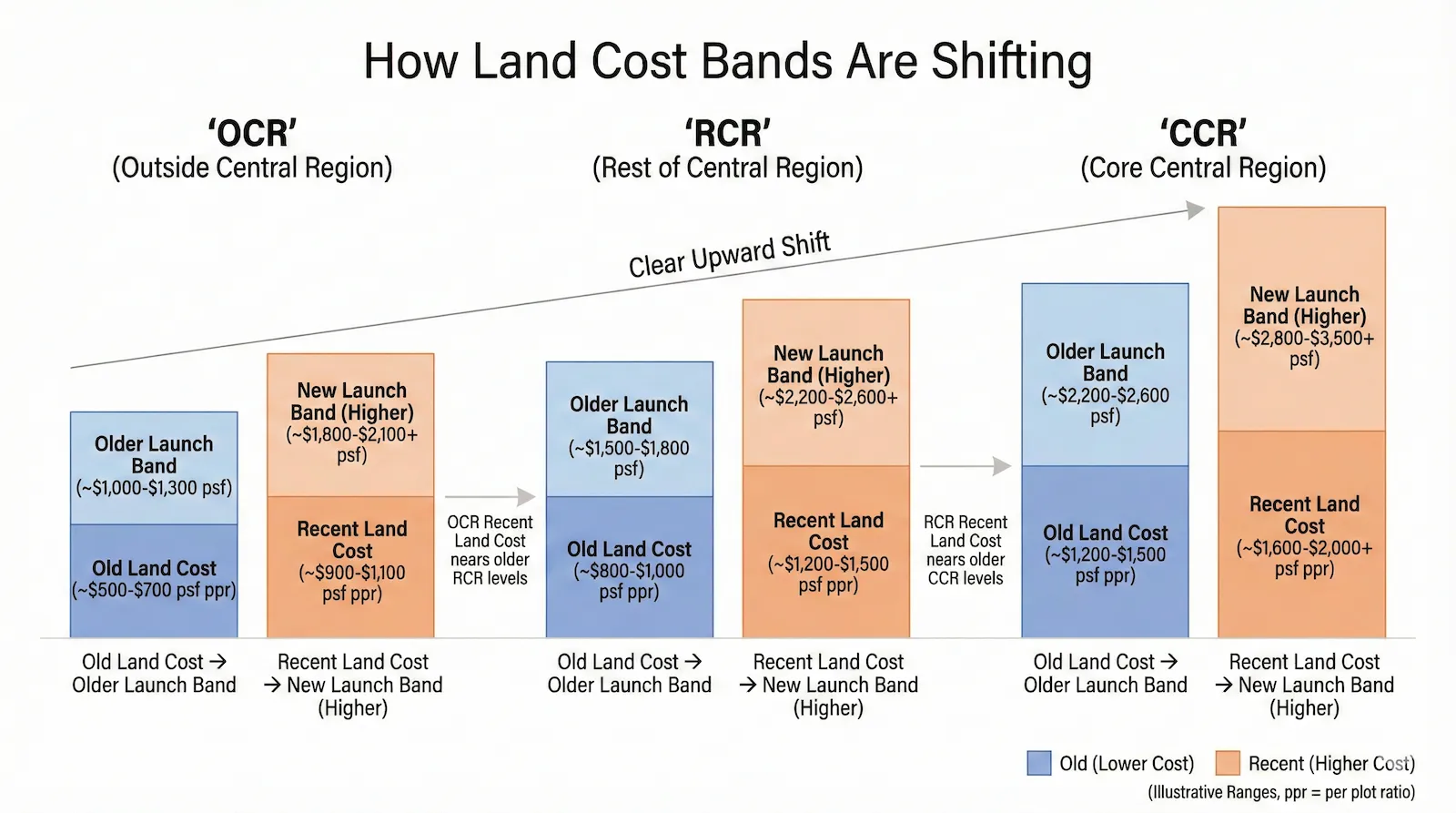

3.3 Macro View – CCR, RCR & OCR Land Cost Bands

Up to now we've looked at land cost project by project.

It's also useful to zoom out and see the bigger pattern across CCR, RCR and OCR.

Traditionally, buyers think of it this way:

- CCR (prime / city) – always the most expensive

- RCR (city fringe) – middle band

- OCR (heartland)—"mass market" and usually cheapest

But the recent GLS tenders are telling a different story.

Recent GLS tenders show CCR, RCR, and OCR land bands shifting up together—the gaps between regions are much narrower than before.

If you look at the land cost slide for CCR / RCR / OCR, you can see that the gaps between the three bands have narrowed. RCR land cost has crept up towards older CCR levels, and OCR land cost has crept up towards older RCR levels.

In simple terms:

- CCR land today supports $3,0xx+ psf type launch pricing for many prime new projects.

New CCR sites like Skye at Holland and River Green support launch prices around $3,0xx psf – a new benchmark for prime projects.

- RCR land is no longer "cheap"—it sits not far below CCR, so many future RCR launches will naturally aim closer to CCR psf.

RCR and even OCR land costs are now much closer to CCR – future launch bands are likely to settle higher, not revert to old levels.

- OCR land is now buying at what used to look like RCR levels, so the next wave of "mass-market" launches will not feel like old-school OCR pricing anymore.

Across CCR, RCR and OCR, newer land cost bands are pushing the next wave of launches into higher psf ranges.

From a buyer's point of view, this means:

- The "new mass-market" OCR is likely to launch at prices that look closer to yesterday's RCR.

- The "new RCR" can end up priced not far from what many people still think of as CCR territory.

If your mental anchor is still "OCR must start with 1 or low-2 thousand psf", these new bands will feel expensive.

But from the developer's perspective, they are simply pricing off higher land costs in all three regions, not just "marking up anyhow".

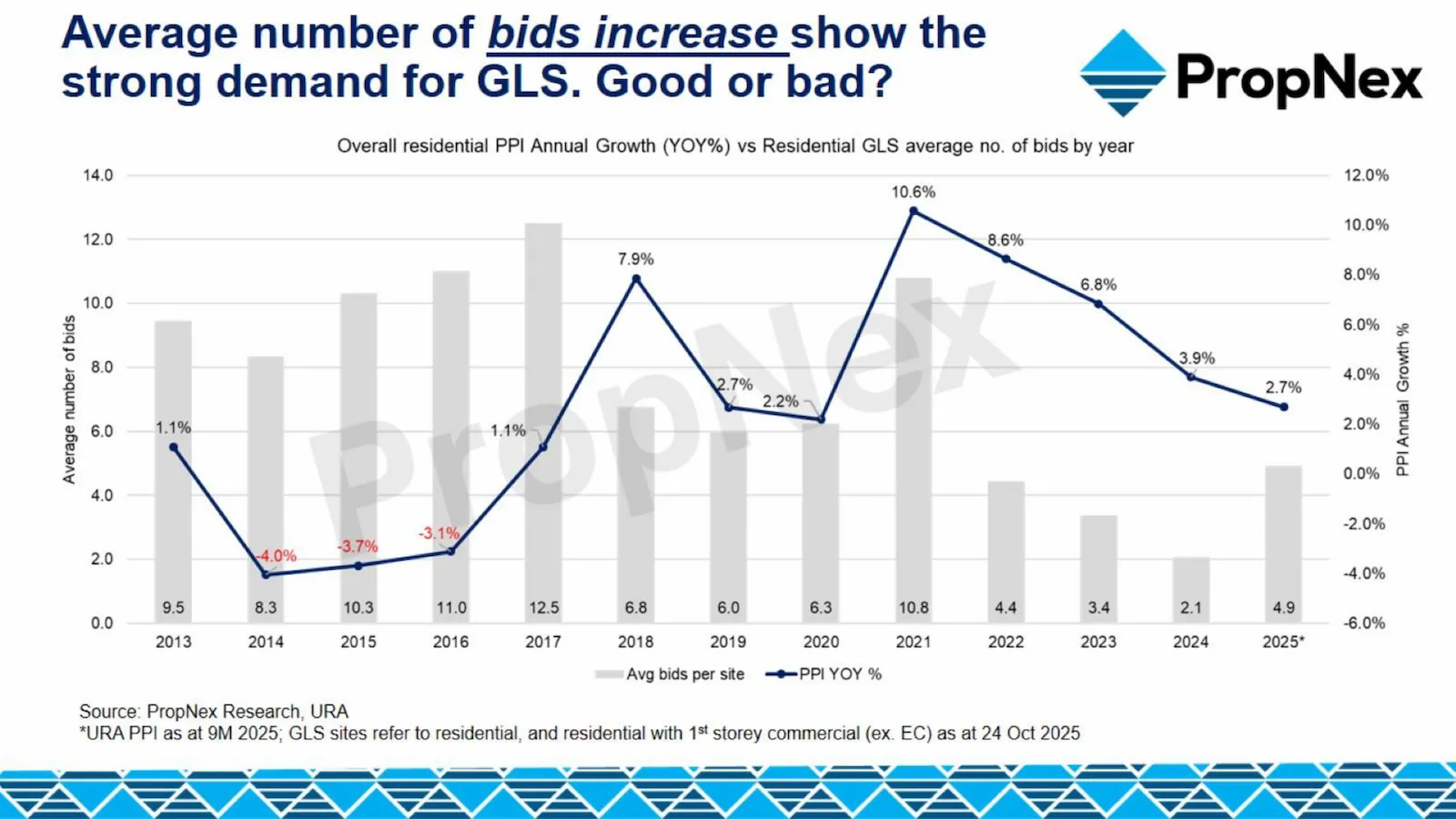

More bidders and firmer GLS bids show that developers still see value at today's land prices.

Higher bid participation reflects stronger developer competition and reinforces the land-cost floor.

3.4 Falling Inventory Of Available Units

Land cost is one side of the story. The other side is how much stock is left.

Two things have been happening quietly in the background:

- Unsold inventory is coming down.

After heavy launch activity in 2023–2025, many projects have sold steadily. There are fewer unsold units sitting on developers' books, especially in good family-sized OCR/RCR projects. - Developer land banks are thinner.

With many sites already launched, developers need to re-stock land if they want projects to sell in 2027–2029. That means more interest—and more competition—for each new GLS site.

Unsold inventory has been drawn down—especially in good family projects—limiting how much 'cheap' stock is left in the system.

On top of that, the chart below shows:

- More bidders per GLS site, and

- Bids clustering at higher psf ppr for well-located sites.

This tells you that developers are still actively competing for land. When:

- Unsold stock is lower,

- Land banks are smaller, and

- Genuine demand is still there.

It is hard for land prices to drop sharply unless there is a major shock.

3.5 What This Means for You as a Buyer

Putting everything together:

- Projects selling now

Many are still based on older, cheaper land—especially buys from 2022 or early 2023. Early phases can offer relatively better entry points for their locations. - Projects launching from 2026 onwards

These are anchored to higher 2024–2025 land costs across CCR, RCR and OCR. Their launch psf will likely set a new band rather than go backwards. - Supply is not overflowing

Unsold stock has been coming down, especially in family-sized units that most Singapore households actually want. - Developers still need land

Land banks must be rebuilt, and competition for good GLS sites remains healthy.

PropNex highlights why "new vs resale" remains a real decision in 2026: the price gap can stay meaningful, so resale is not "second best." At the same time, with land costs stepping up, future launches can defend higher pricing bands. That's why "waiting for a dip" sometimes means meeting the next band, not a cheaper one — and why we shortlist by fundamentals, not headlines.

The disciplined-shortlist principle is visible in the launch data too. Our Pinery Residences review deconstructs why the March 2026 launch cleared 92.5% of inventory at $2,546 psf — the buyers passed the fundamentals filter and recognised the entry baseline was set by the land cost, not the showflat staging.

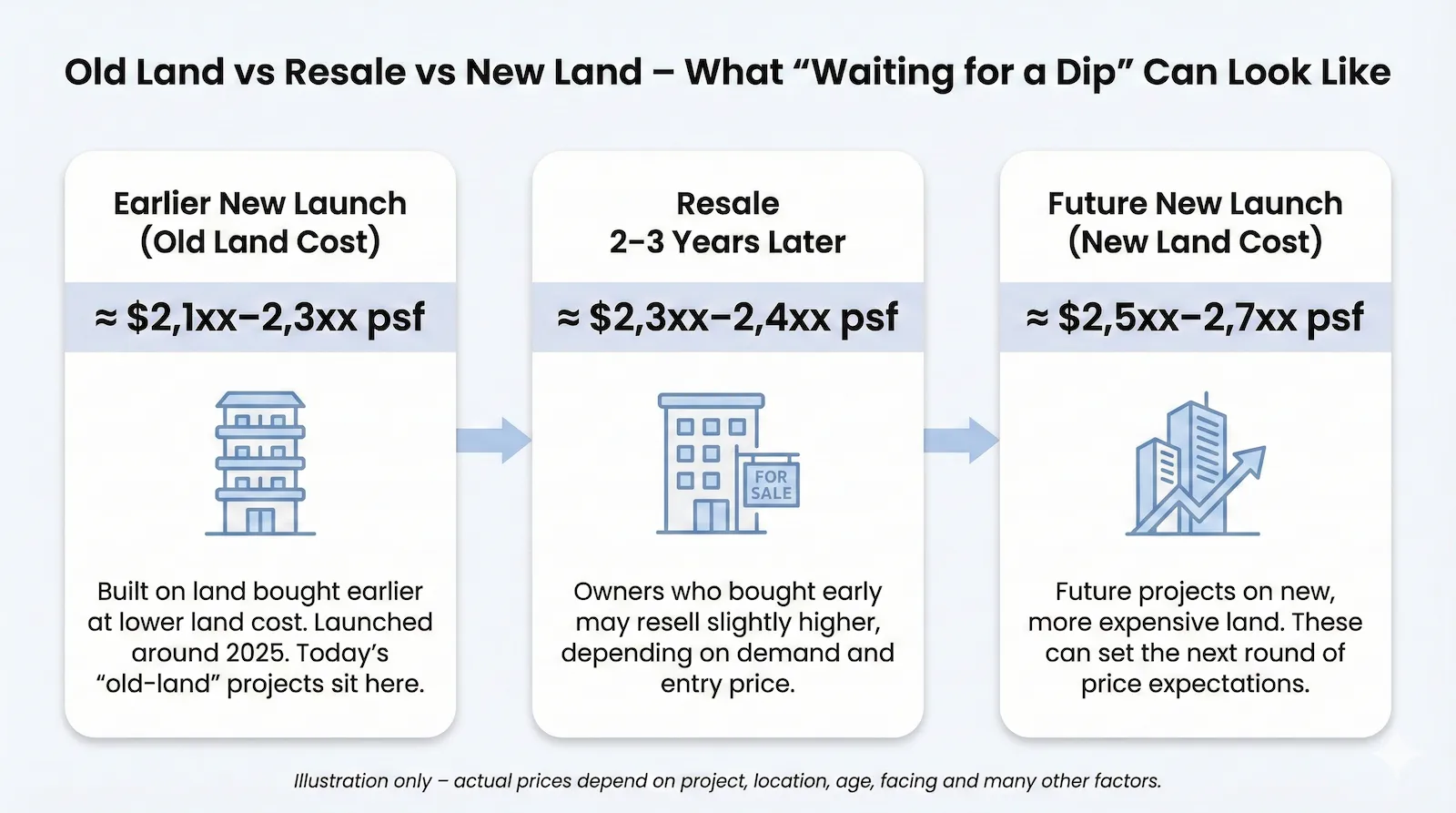

Here's a simple, made-up example to show what this old-land vs. new-land story can feel like in real $ psf terms. The numbers are for illustration only, but they help you see the bands more clearly.

For serious buyers, the takeaway is not "sure, confirm, must buy now."

The real takeaway is:

If you are waiting for land prices to reset back to 2017–2019 levels, you may be waiting for a world that probably won't come back.

A more realistic question is

- Which projects still based on older land costs make sense for us?

- Which upcoming launches do we want to benchmark against so we don't only wake up when the new price band has already become normal?

This doesn't replace your own affordability checks and plans.

It simply explains why the starting point for future launch prices is shifting and why 2026 may be one of the last windows where "old land" and "new land" projects still overlap in the same market.

Illustration only—how an earlier "old-land" launch, a later resale, and a future "new-land" launch can sit at three different price bands. Sometimes "waiting for a dip" simply means meeting the next, higher band instead.

Unlock the Full Strategic Blueprint

Enter your details below to instantly decode this analysis. Your device will receive a secure, 30-day VIP pass to automatically bypass all future gates across our intelligence network. Zero duplicate entries required.

4. Property Financing & Interest Rates: Pain, Relief, and Monthly Instalments

Interest rates are no longer a valid excuse for paralysis; they are a known mathematical variable that dictates your holding costs.

4.1 The Mathematics of Predictability

While the 4%+ peaks of recent years created genuine friction, the current stabilization of SORA means your monthly holding cost is now highly predictable. Whether you are running condo downpayment calculations 2026 for a new launch or a resale unit, a Calculated Entry Strategy requires stress-testing your loan at +1% and +2% above today's rates. If your household income can absorb that buffer, the math gives you the green light to execute.

4.2 Painful Highs vs Today's Range

Recently, we came through a period where many packages were above 4%. That was painful, especially for big loans.

Today, we are back to a more reasonable band—not as cheap as COVID, but not as painful as the recent peak. This is why I often tell clients:

"You're no longer buying at the rate peak. You're buying with eyes open and planning for a range."

4.3 How to Think About Packages

Without going into product details (banks will always have new packages), a few simple rules:

- Don't just chase the lowest teaser rate—look at how it resets.

- Avoid over-stretching your loan just because rates feel low now.

- Always ask: "At +1–2%, am I still OK?"

We'll come back to these in Section 9 (Financing Safety Nets).

4.4 "Am I Too Late?" – Buying After Prices Have Moved

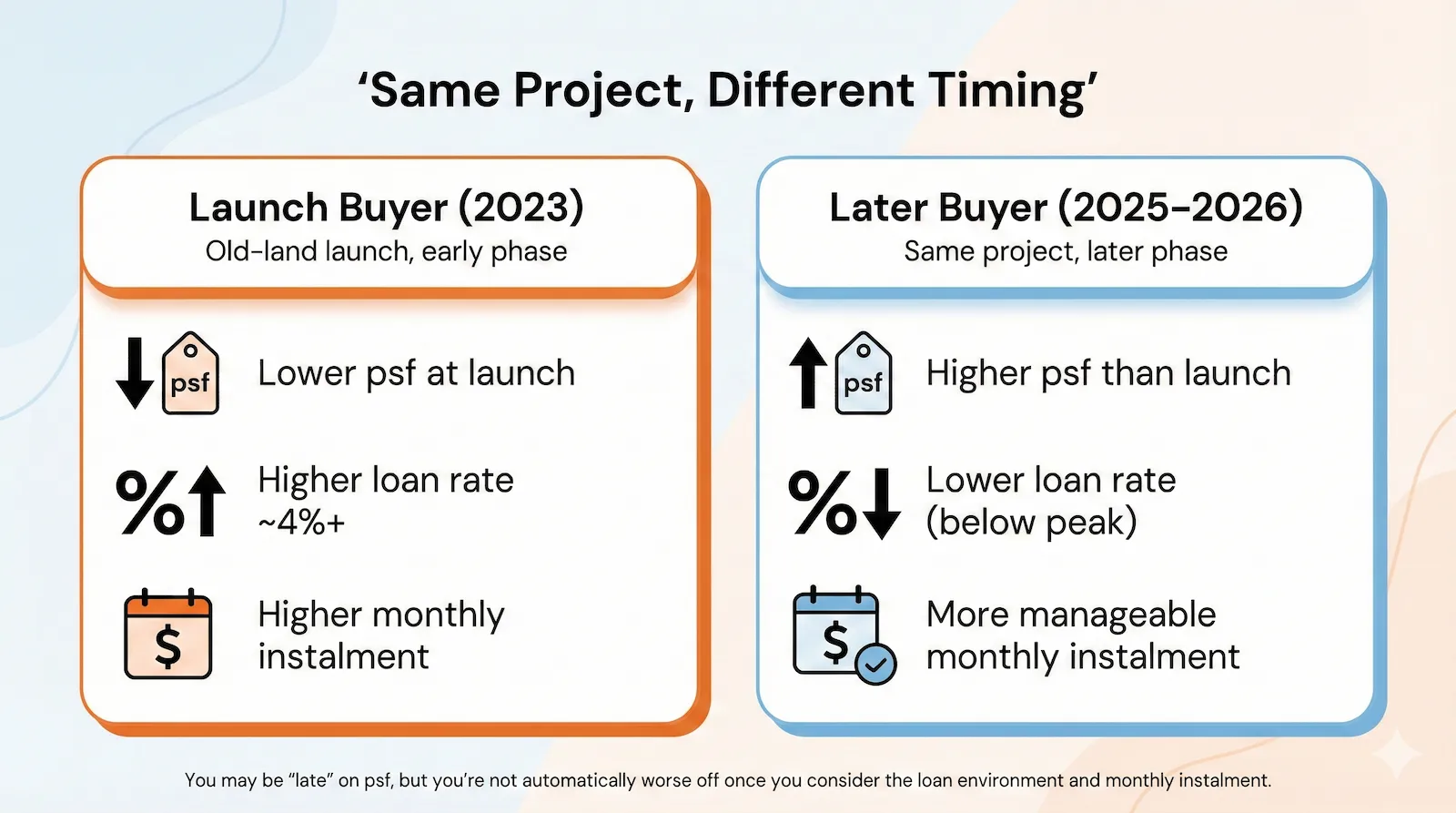

A very common worry I hear is:

"Sam, I know this is an 'old-land' project and the story makes sense... but launch was in 2023. Price has already moved up. I'm paying more than the early buyers. Am I too late?"

It's true that early buyers usually get the lowest psf in the project. If you walk in one or two years later, you're often looking at later stacks or higher phases.

But there's another piece most people forget: what interest rate those earlier buyers were paying.

Same project, different interest environment

Imagine two couples buying the same project:

- Couple A bought in 2023, early phase

- – Lower psf at launch

- – But they took a loan when floating packages were around 4%+

- Couple B buys in 2025 or 2026, later phase

- – Higher psf than launch

- – But they're taking a loan in a lower rate band (not COVID-cheap, but clearly below the 4% peak)

Over the first few years of the loan, Couple A may easily pay tens of thousands more in interest than Couple B – even though their psf is lower.

I'm not saying it's "better" to buy later. The point is simply this:

You're not automatically at a terrible disadvantage just because you weren't there on launch day.

You have to look at both:

- the price you pay, and

- the loan environment you're paying it in.

What this means for you

If you're considering an old-land launch today and worried you're "late":

- Don't just compare your psf to launch psf.

- Also compare your monthly instalment at today's rate versus what it would have been at 4%+.

- Ask: "For our income and buffer, is this instalment still within our comfort band?"

In other words, focus less on beating the earliest buyer, and more on whether you're entering at a sensible combination of price and loan cost that you can comfortably hold for 7–10 years.

We'll get more practical about this in the next chapters: for HDB upgraders, home buyers and investors, the question isn't "Did I buy at the lowest psf?" It's "Does this purchase still make sense for my numbers and season of life, today?"

Same project, different timing: early buyers got lower psf, but many were paying 4%+ interest. Later buyers may pay slightly higher psf, but at a lower rate and more manageable monthly instalment.

5. The HDB Double Wave: Sale Equity vs MOP Supply Through 2028

If you own an HDB today, the most dangerous strategy is assuming your flat's value will remain static while you wait. You are currently operating inside the HDB 'Double Wave'—a mathematical collision of peak unrealized equity and an impending supply shock.

Two data points are moving against each other simultaneously:

- The Equity Peak: Your current HDB valuation, which is highly vulnerable to the HDB MOP 2026 supply surge.

- The Target Price: What a suitable private condo will cost once more 'new land' launches set higher psf benchmarks.

If you hold your flat to squeeze out the last bit of upside, your upgrade gap compounds against you. Mapping your exact sell HDB buy condo timeline today is a mathematical necessity to prevent bridging loan stress and secure a seamless transition.

5.1 The "Double Wave" Mechanics: Wave 1 Past Gain, Wave 2 MOP Supply

Think about the HDB story this way:

- Over the last cycle, HDB resale prices have already run up strongly. Many owners are sitting on solid paper gains.

- From 2026 onwards, a big batch of newer BTO flats will reach MOP. More flats become eligible for resale in a short window.

- On top of that, any future tweaks to policies (for example, the 15-month wait-out rule or other measures) can influence how many people move between HDB and private.

This is what "double wave" looks like with numbers: the market can stabilise overall, while strong pockets remain strong (mature towns, bigger flats, high demand). At the same time, the MOP wave adds more supply and choice from 2026 onwards — which tends to reduce panic conditions and make the upgrader timeline more sensitive (sell-first vs buy-first planning matters more). When you are planning this carefully, mapping your exact sell HDB buy condo timeline is the difference between a smooth transition and getting caught with a widening upgrade gap.

Put simply:

- Wave 1 is the past price gain you're already sitting on.

In the last cycle, HDB moved faster than private in percentage terms—which is why many owners feel "quite shiok" on paper now. - Wave 2 is the upcoming MOP supply (plus policy changes) that could affect demand and pricing.

HDB market stabilisation (Source: PropNex 2026 Property Market Outlook Report).

Together, that can mean:

- HDB prices stabilize or flatten in some towns and flat types, especially where many similar units hit MOP at the same time.

- Private condo prices, especially in OCR/RCR family projects, stay firm or move up as new land costs reset launch benchmarks.

For an upgrader, that's a classic squeeze:

- Your starting point (HDB value) may have less support going forward.

- Your target (condo price) has more reasons to stay firm or rise.

That's why 2026–2027 behaves like a window rather than just "business as usual".

A large batch of newer flats will reach MOP from 2026 to 2028—that's Wave 2 of the HDB double wave.

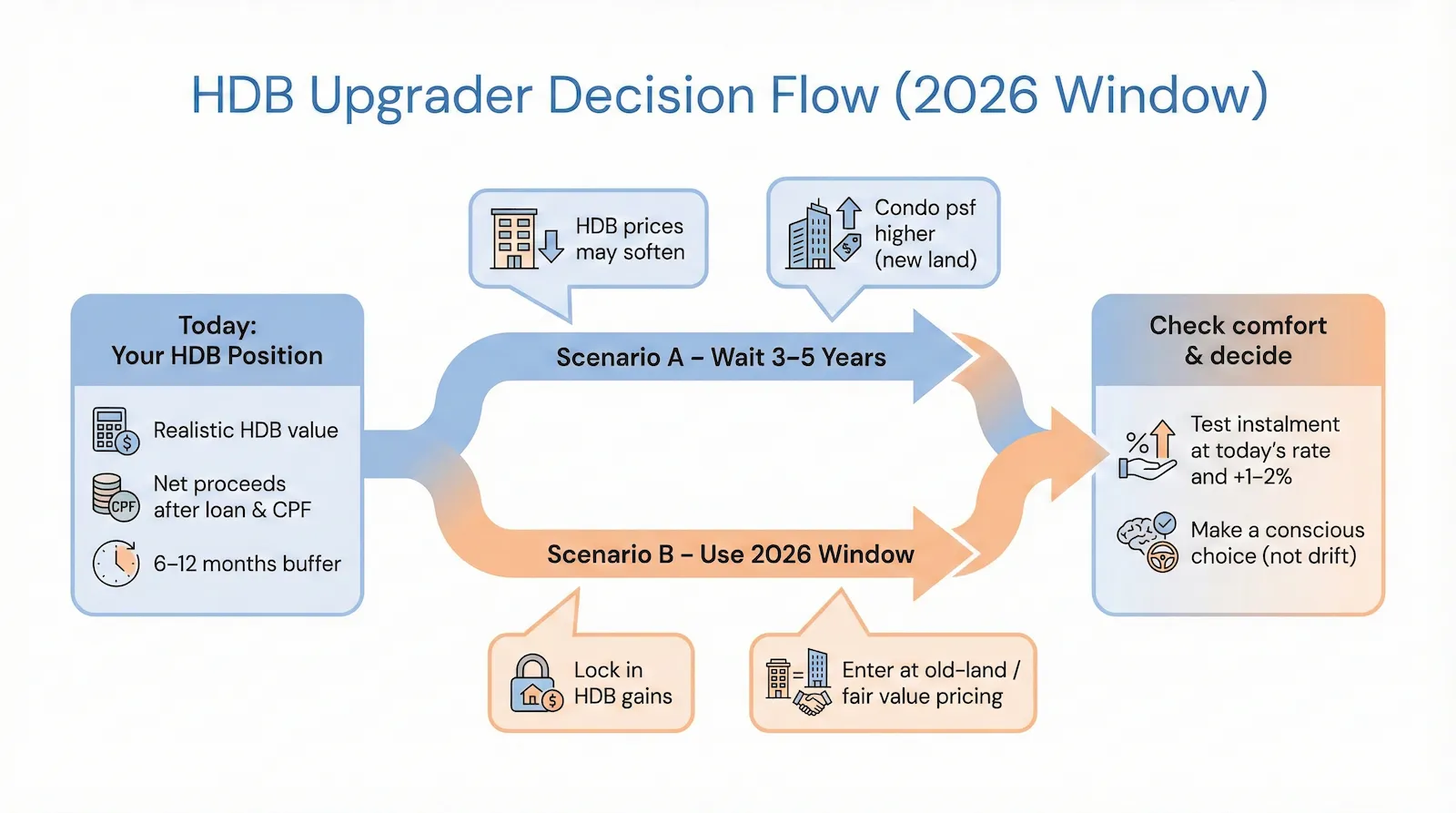

5.2 Scenario A vs Scenario B – Don't Drift

A simple way to frame your decision is to compare two clear paths.

Step 1: Know your numbers today

- Get a realistic HDB valuation (not just the most aggressive agent quote).

- Work out your net proceeds after outstanding loan and CPF refund.

- Check that, after upgrading, you would still have 6–12 months of emergency buffer.

Step 2: Draw your own Scenario A vs Scenario B

- Scenario A – "Wait 3–5 years"

- – What if my HDB sells a bit lower when more MOP flats appear?

- – What if OCR/RCR condo prices are higher by then because of new land launches?

- Scenario B – "Use 2026 window"

- – What if I sell while HDB prices are still firm,

- – And buy into an old-land launch or fair-value resale before the next round of benchmarks is set?

Step 3: Check your comfort level

In both scenarios, ask:

- Can I handle the monthly instalment at today's rates and at +1–2%, with a proper buffer?

- If the numbers say I can upgrade safely now, but I'm still waiting "just in case prices crash," is that really a numbers issue—or a psychology issue?

The goal is not to rush you.

The goal is to make sure you don't drift, then wake up a few years later to find that the window has quietly closed.

Choose wisely

5.3 "Win Small, Lose Big"—A Common Upgrader Trap

Many upgraders are so afraid of "losing money" that they end up winning small and losing big.

It often looks like this:

- You hold on to an older HDB because it feels "safe" and maybe even fully paid.

- You keep saying, "Wait a bit more; maybe we can squeeze another $20–30k."

- At the same time, better-located condos based on older land costs get taken up, and newer launches are priced off higher GLS land.

Holding out for a small extra gain on your flat can quietly widen the upgrade gap and delay your lifestyle upgrade.

On paper, you didn't "lose"—you still own your flat.

In reality, three things may have happened:

- Your upgrade gap quietly widened.

The condo you wanted is now further out of reach, even if your HDB value didn't crash. - You missed a strong window for choice.

The best stacks and layouts in good projects were snapped up while you were "seeing how." - Your lifestyle gains were delayed.

Extra space, facilities, schools, and location—all pushed back by a few more years.

That's what "win small, lose big" really means for an upgrader:

you avoided a small, short-term risk… but gave up a much larger, long-term opportunity.

The point is not to chase every upgrade just because the window exists.

The point is to be honest: if the math shows you can upgrade safely, "doing nothing" because of fear can quietly cost more than moving carefully.

5.4 Worked Example: Punggol 4-Room to $2M OCR 3-Bedder

(Numbers here are for illustration only – every case will be different. When you upgrade to condo singapore downpayment calculations must factor in not just headline prices, but also your locked CPF funds, cash-on-hand, and how your HDB sale proceeds flow into the new purchase.)

- Current: 4-room HDB in Punggol

- – Likely sale price: $750k

- – Outstanding loan + CPF refund: $400k

- – Net proceeds ≈ $350k

- Target: 3-bedder OCR condo at $2.0M

- – Loan needed: ≈ $1.5M

- Today's rate (≈1.7%) → instalment ≈ $6,100/month

- At +2% (≈3.7%) → instalment ≈ $7,500/month

If Mr. & Mrs. Tan can comfortably handle $6,100 now and still cope at $7,500 if rates climb, with 6–12 months of buffer after moving, they likely have a viable upgrade.

Run your own version of this stress test through the Gap Decoder affordability calculator before booking a unit.

Their question should not be

"Will prices crash 20%?"

Their real question is

"If the numbers say we're safe, are we willing to use this window — or do we prefer to wait and accept a bigger upgrade gap risk later?"

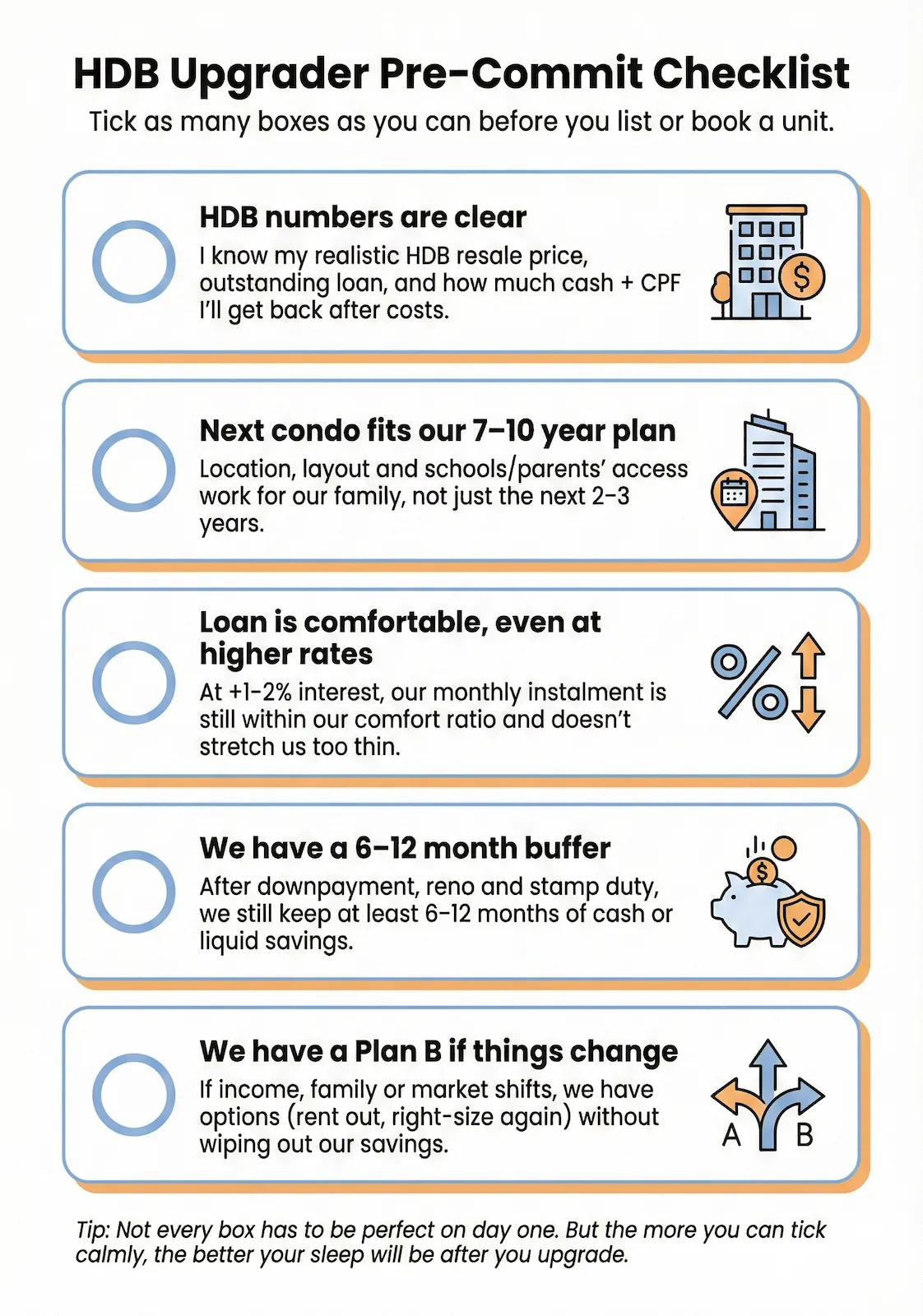

Below is a simple HDB Upgrader Pre-Commit Checklist you can screenshot or print. Tick as many boxes as you can before you list or book a unit.

Use this checklist as a quick filter—if you can't tick most boxes calmly, strengthen your numbers first before upgrading.

6. Safe Entry Math: Housing Ratio, Buffer and Layout Filters

If you are transitioning from renting, or executing an upgrade to condo singapore strategy from a smaller private unit, your risk profile is distinct from an HDB upgrader. You possess capital flexibility, but lack the unlocked equity of a public housing sale.

The primary threat is not market timing; it is structural over-leverage. A Calculated Entry Strategy requires mathematically defining your safe band before viewing properties. For most households, a total housing ratio below 35-40% of gross income provides the necessary buffer to protect your capital against volatility.

PropNex chart reminder: "stable market" doesn't mean every segment moves the same. Use this as a context anchor — then decide your safe band. (Source: PropNex 2026 Property Market Outlook Report).

6.1 Define Your Safe Band

A healthier approach: if you're buying direct from a developer, that includes understanding the progressive new launch condo payment schedule so you know exactly when each stage of cash and CPF will be deducted.

- Decide your own comfort limit – for most households, a total housing cost ( + basic running costs) of below about 35–40% of gross household income is a good reference point, not a hard rule.

- Protect your buffer – make sure you still have 6–12 months of essential expenses as an emergency buffer after all buying costs (BSD, legal, basic renovation). If this buffer is not there yet, building it should be your first step.

- Use bonuses to strengthen, not stretch – treat any bonus or extra income as a buffer builder, not as "extra budget" to stretch the loan. Use windfalls to shorten your loan or fatten reserves.

- For condo upgraders: decide upfront whether you will sell then buy, or buy then sell. Understand any ABSD exposure, bridging loan needs and how many months of overlap you can comfortably handle if both properties are on your books for a while.

6.2 Aim for a 5–7 Year Home, Not a 1–2 Year Flip

In today's environment (with SSD at 4 years), a safe plan is to buy a home you can comfortably hold for at least 5–7 years.

Choose a unit you're happy to stay in even if you don't upgrade again quickly. That means:

- Enough space for your near-term family plans (potential kids, WFH, aging parents).

- A commute and daily routine you can live with.

- A location with basic amenities – supermarket, food, transport, schools – not a "desert island" condo where every small errand becomes a hassle.

If your plan only works when you can sell in 2 years for big upside, that's not a plan – that's a gamble. You want a home that works for your life first, and for returns second.

6.3 How to Choose a Condo Floor Plan: Real Options vs. Fantasy

It's fine to walk into super-prime showflats and dream a little. But your serious shortlist should be made up of projects you can actually buy and live in, not just the aspirational ones. Evaluate the resale condo vs new launch 2026 landscape carefully—sometimes an older resale offers immediate space and location advantages, while a new launch provides a more structured entry price and payment path.

Focus your shortlist on:

- Projects and unit types that fit your numbers today, not only "if my income doubles".

- Units with realistic resale demand – e.g. sensible 2BR and 3BR layouts near jobs, MRT or schools – not ultra-niche or awkward configurations that future buyers will skip.

- A mix of new launches and resale options that give you some price buffer versus nearby comparables (we can run those numbers together).

Remember: "Not now" is also a decision.

If the numbers are too tight, it's perfectly valid to pause intentionally and strengthen your position, instead of half-looking and half-hoping.

Whether you're a first-time buyer or a condo upgrader, the next condo you buy doesn't have to be your "forever" home. But it should be a strong, comfortable step – not a constant source of stress.

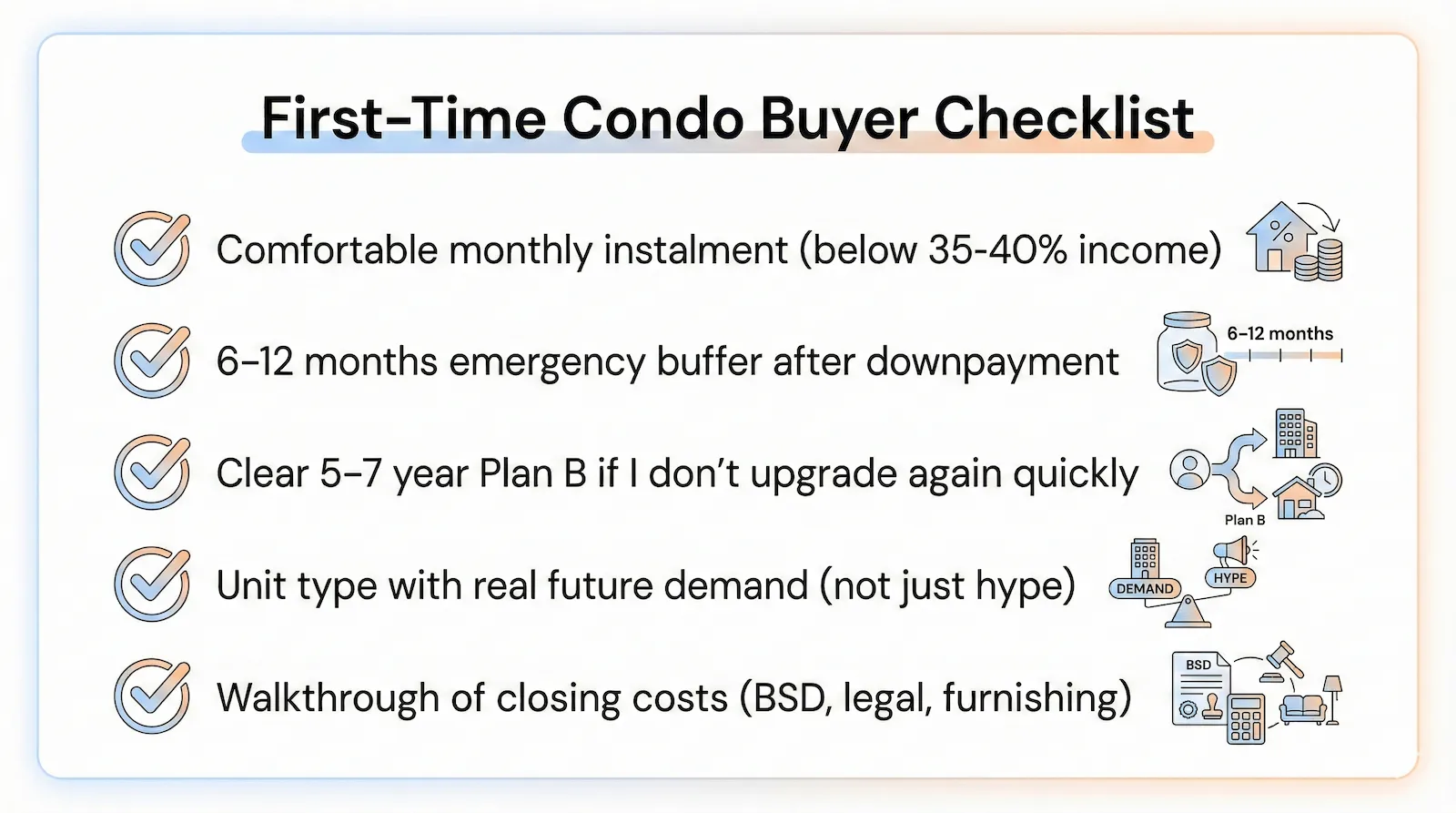

Use this checklist diligently, then pair it with the "First-Time Condo Buyer Checklist" visual below as a quick recap before you commit.

Make sure every box is ticked.

7. Exit Planning for Second-Property Buyers: 7-10 Year Horizon

For investment units, the primary metric is not basic affordability; it is capital efficiency. In a landscape of elevated ABSD and rigid financing guidelines, every deployment of capital must be mathematically justified.

Before deploying capital, you must validate the structural Upside/Value. A Calculated Entry Strategy demands a clear exit narrative: Who is your target buyer in 7-10 years, and what macroeconomic drivers will compel them to pay a premium? If you cannot mathematically prove the future demand and absorb projected vacancy periods, the asset fails the stress test.

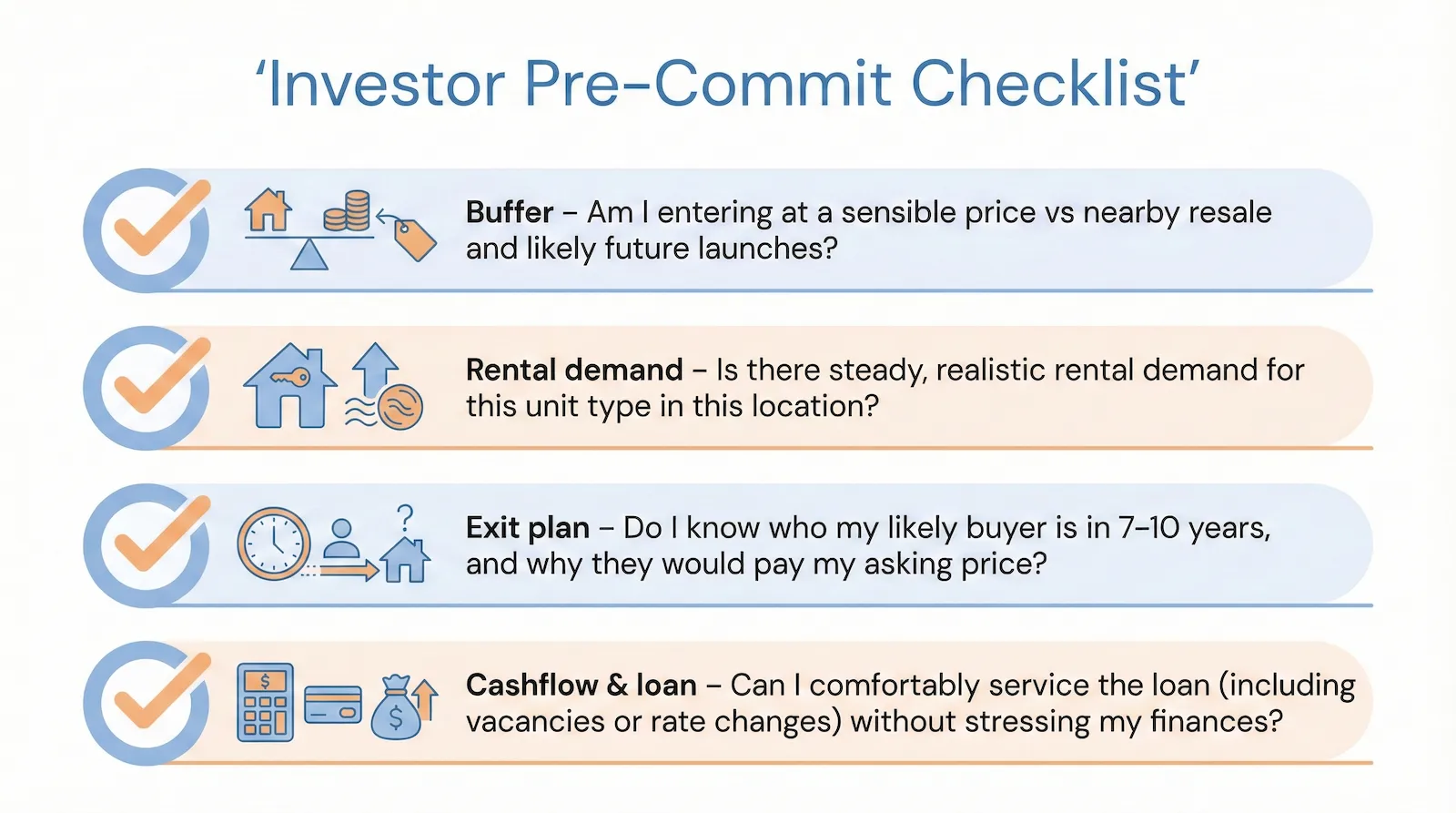

7.1 The Investor Pre-Commit Checklist (Expanded)

Use this simple four-part checklist before you sign any Option:

1) Buffer & entry price

- Am I entering at a sensible price compared to nearby resale and likely future launches?

- After paying BSD, legal, reno and allowing for some vacancy, do I still have a decent cash buffer?

2) Rental demand

- Is there steady, realistic rental demand for this unit type in this location (near jobs, schools, MRT, amenities)?

- Have I looked at actual past rents and vacancy, not just "sure can rent one" talk?

3) Exit plan

- Who is my likely buyer in 7–10 years, and why would they pay my asking price?

– Upgraders? Parents buying for children? Downsizers? - If you can't clearly picture your future buyer, your exit is unclear.

4) Cashflow & loan

- Can I still comfortably service the loan if:

– rent dips, or

– there are a few months of vacancy, or

– interest rates creep up by 1–2%? - If any of these make you very nervous, the position may be too tight.

Simple rule:

If any of these four boxes is "don't know" or "honestly, no", slow down. You're better off waiting and preparing than forcing a weak investment just because everyone around you is buying "something".

Good investments are usually boring and repeatable, not exciting and sleepless.

If you can't tick all four boxes confidently, the investment probably isn't ready yet

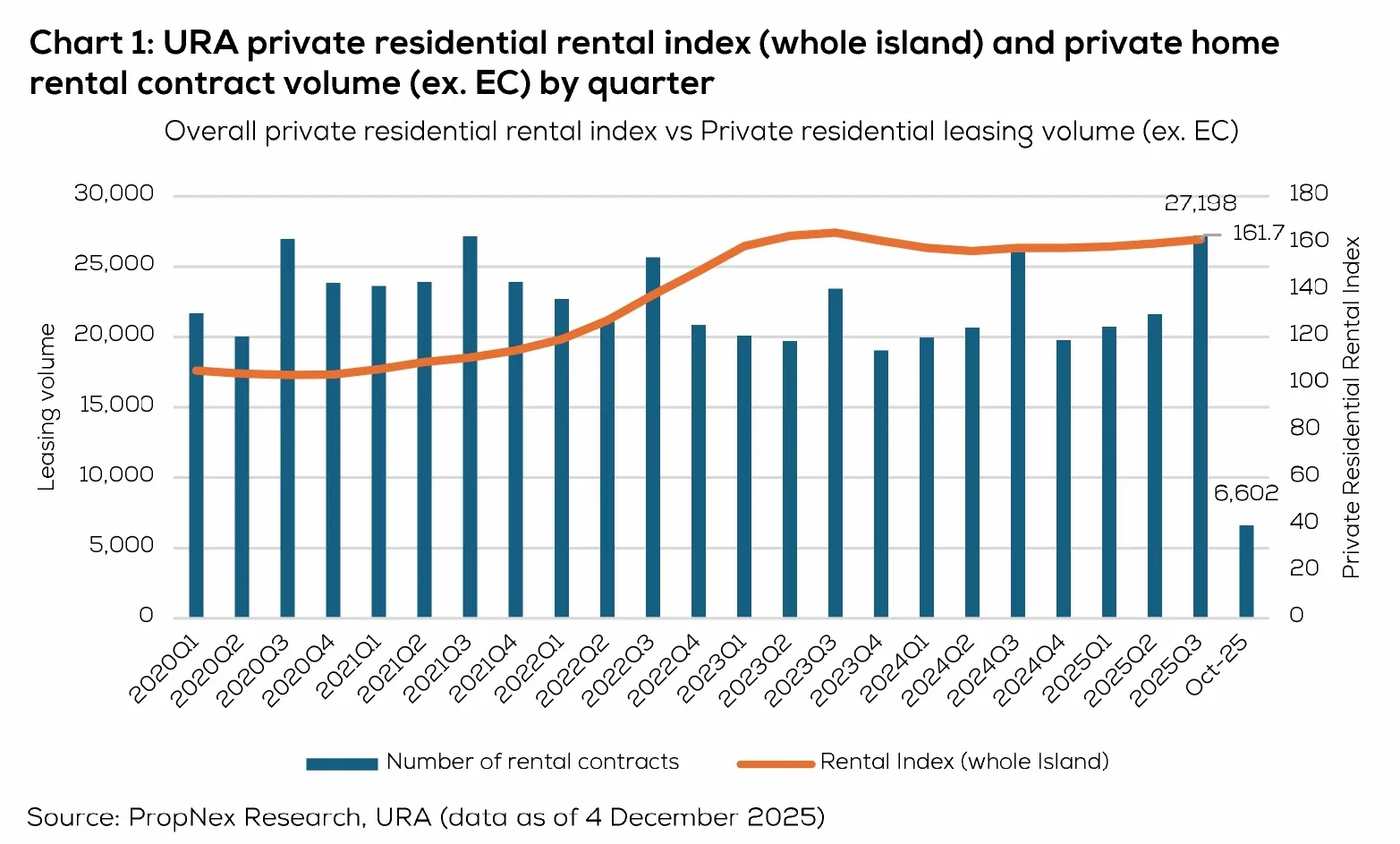

For investors, 2026 is less about "hope rent keeps jumping" and more about buying an asset you can hold comfortably even if rent is flat for a period. PropNex's leasing/rental charts support a simple investor discipline: assume conservative rent, plan vacancy, and stress-test instalments — then only buy if the deal still works.

Rental is still supportive — but don't underwrite like the peak years.

The rental market has recovered, but the data suggests a more cautious phase: leasing volume and rental index trends are stabilising while more supply is still coming through. For investors, this is why the deal must work even if rent stays flat, dips slightly, or you face a normal vacancy period — not because you "hope rent keeps jumping".

(Source: PropNex 2026 Property Market Outlook Report).

Practical takeaway: For your stress test, assume a conservative rent (not best-case), and budget for vacancy — for example 1–3 months of vacancy in each of the first 2 years — then proceed only if you're still comfortable.

Rental reality in 2026. (Source: PropNex 2026 Property Market Outlook Report).

7.2 "Win Small, Lose Big"—A Common Investor Trap

Many Singaporeans are very scared to lose big, so we try to "play safe". Ironically, this can lead to winning small and losing big instead.

Typical pattern:

- You hold on to an older HDB or a small, average investment unit because it feels safe and maybe even fully paid.

- You refuse to explore a better-located upgrade or stronger investment because "price already very high" or "later then see".

Fast forward 5–10 years:

- The better asset (strong location, better tenant / upgrader demand) has grown nicely in value and rent.

- Your "safe" asset has moved much less, or even become harder to sell as newer supply comes in.

On paper, you "didn't lose money".

In reality, you may have lost the chance to:

- Build a stronger equity base

- Ride on better future demand and launches

- Improve your family's quality of life

The goal is not to "chiong" every opportunity or over-leverage.

The goal is to avoid getting stuck in an asset that quietly limits your options for the next decade.

When we sit down together, we'll look at your portfolio and ask:

- "If I hold this asset 7–10 more years, is it helping me win big enough, or just win small and lose big on opportunity cost?"

Sometimes, the bravest thing is not to buy more, but to re-structure what you already own so your next move actually moves the needle.

8. ABSD, TDSR & Policy Guardrails: "What If I'm Wrong?"

Policy guardrails are not arbitrary restrictions; they are structural market stabilizers designed to mathematically prevent systemic over-leverage. A Calculated Entry Strategy requires operating efficiently within these boundaries, not stretching to their absolute limits.

The Calculated Reality: ABSD, TDSR, and SSD mathematically filter out speculative capital, drastically reducing the probability of a sudden market crash. You must stress-test your baseline affordability against these exact policy constraints. If a sudden policy tightening or personal income shock breaks your holding power, your capital deployment is structurally flawed.

8.1 Key Policy Guardrails

TDSR (Total Debt Servicing Ratio)

- Caps your total monthly debt repayments as a percentage of income.

- Reduces the chance of mass forced selling from over-leveraging.

- In simple terms: even if you feel you can stretch, TDSR is there to stop you from doing something dangerous on paper.

ABSD (Additional Buyer's Stamp Duty)

- Discourages speculative multiple purchases.

- Makes "anyhow buy a few units" painful and filters out casual speculators.

- For most genuine upgraders and first-timers, the main question is whether you can avoid ABSD or when it will kick in if you keep one more property.

SSD (Seller's Stamp Duty)

- Applies if you sell within the first 4 years.

- Encourages longer holding and reduces quick flips in the resale market.

- It's one more reason your plan should be built around a 4–7 year holding horizon, not a "sure can sell higher in 1–2 years" mindset.

These rules don't freeze prices, but they reduce the extremes—especially compared to markets with very loose borrowing and no stamp duties. They are part of why Singapore tends to see controlled pullbacks and sideways periods, rather than full-blown crashes every few years.

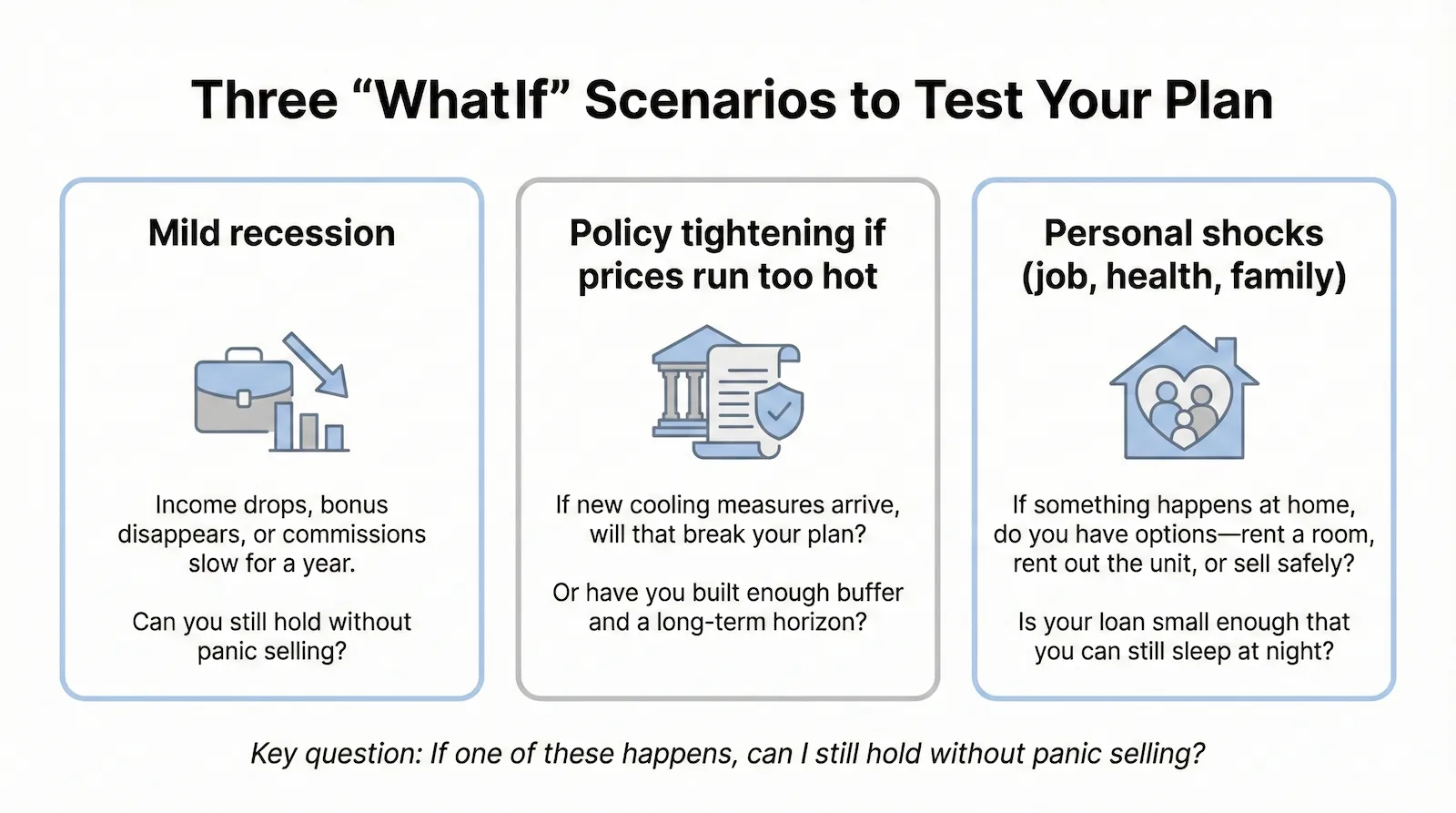

8.2 Risk Scenarios to Think About

Before you commit, it's worth asking yourself how your plan holds up under a few common "what if" situations:

Mild recession

- If your income drops, your bonus disappears, or your commissions slow for a year, can you still hold without panic selling?

- Would you need to slash your lifestyle, or is it uncomfortable but still manageable?

Policy tightening if prices run too hot

- If authorities introduce another round of cooling measures, will that break your plan (for example, affect your ability to buy/sell or refinance)?

- Or have you built enough buffer—and a long-term horizon—to ride through policy changes without rushing into bad decisions?

Personal shocks (job, health, family)

- If something happens at home, do you have options—e.g., rent out a room, rent out the whole unit, or sell without wiping out your savings?

- Is your loan size small enough that you can still sleep at night even if life throws you a curveball?

Three common "what if" scenarios to test your plan before you commit.

One simple question to close:

"If one of these happens, can I still hold without panic selling?"

If the honest answer is "yes—with some belt-tightening but still okay," your plan is more robust than many buyers out there. If the answer is "honestly, no," then the numbers are too tight—and we should adjust the plan before you commit, using the financing safety nets in the next section.

9. Property Financing Safety Nets & Affordability Rules

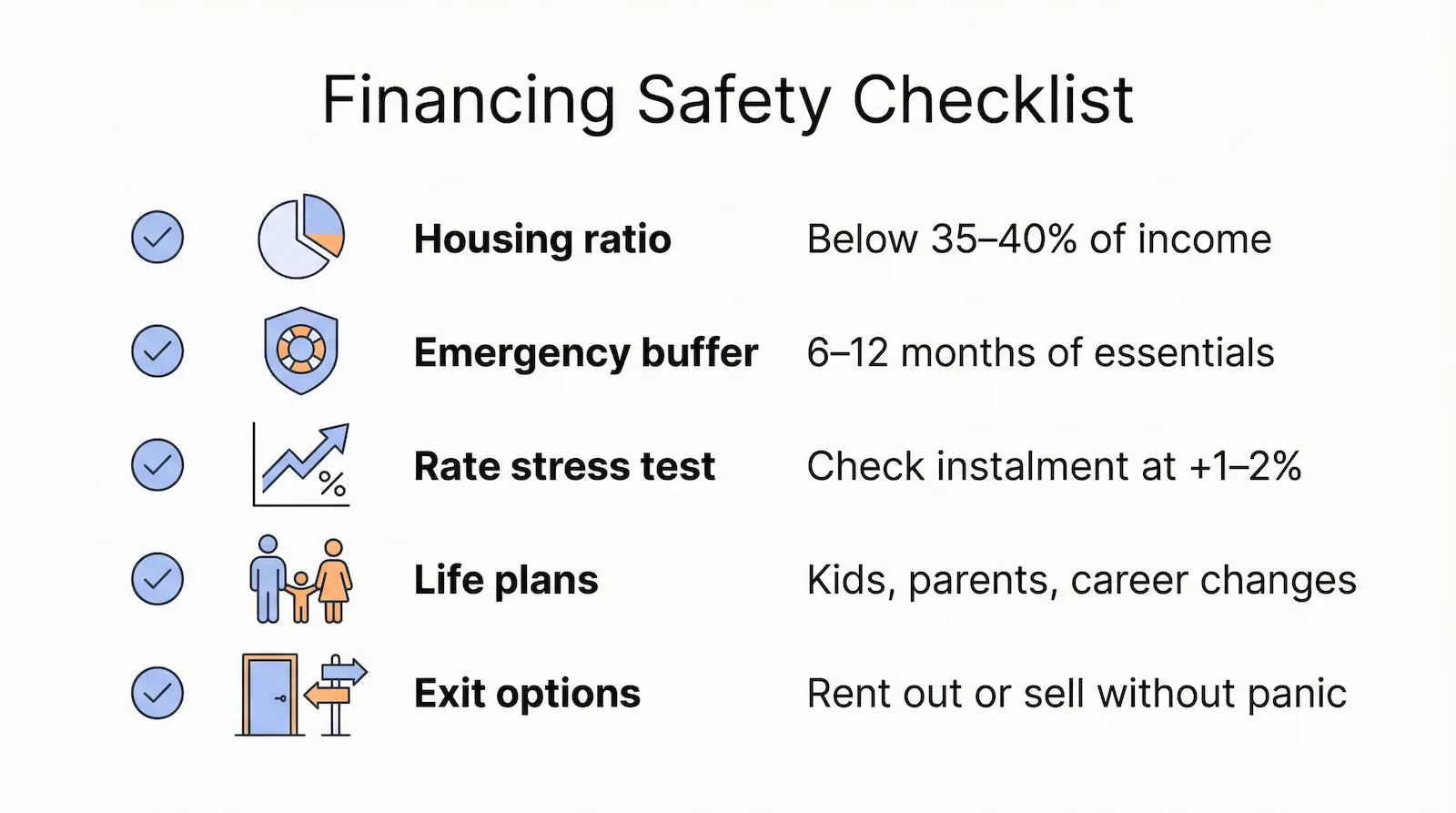

Regardless of your buyer profile, emotional readiness is irrelevant without mathematical validation. This is your definitive pre-commitment filter. You must objectively clear these thresholds before executing any Option to Purchase.

The Calculated Reality: You must mathematically verify five strict parameters before deploying capital: a total housing ratio below 40%, a liquid emergency buffer of 6–12 months post-acquisition, a stress-tested loan trajectory, structural resilience against life transitions, and a clear, quantifiable exit strategy. If any of these metrics fail validation, you must pause and restructure your capital.

9.1 Five Boxes to Tick Before You Say "Yes"

Make sure you can honestly tick these five:

- Housing ratio—After the move, my total housing cost (instalment + basic running costs) is at a level I'm truly comfortable with, not just "bank say can".

- Emergency buffer—After downpayment, BSD, legal, and basic renovation, I still have 6–12 months of essential expenses in cash or safe instruments.

- Rate stress test—I have checked my monthly instalment at +1% and +2% above my starting rate, and I can still manage without major lifestyle pain.

- Life plans—I have thought about upcoming changes (kids, supporting parents, career moves, starting a business), and I'm confident this loan can survive them.

- Exit options—In a worst-case scenario, I have realistic options: rent out a room, rent out the whole unit, or sell without wiping out my savings.

If you can tick most of these calmly, you're standing on much firmer ground—regardless of what the headlines say. If one or two boxes are shaky, it doesn't automatically mean "don't buy". It means pause, adjust, and plan properly before you commit.

9.2 Simple "Back of Envelope" Checks

When we sit down together, we'll usually do quick checks like:

- Housing ratio = (all housing costs ÷ gross household income) × 100%.

Target: ≤ 35–40%. - Buffer = (cash + safe investments after purchase) ÷ monthly essential expenses.

Target: 6–12 months minimum. - Stress-tested instalment—Use an online calculator with the interest rate set 1–2% higher than your initial package to see if you're still comfortable.

These are not bank formulas—they're your own comfort rules. As long as they still look healthy after stress-testing, you're on much safer footing than someone who only asked, "Bank say can or not?"

If you can tick most of these calmly, you're on much firmer ground than most buyers.

10. Singapore Property Buyer Psychology & Decision Traps

Market paralysis rarely stems from a lack of data; it is the direct result of cognitive friction and emotional decision-making. Operating on retail headlines rather than mathematics leads directly to wealth erosion and widening upgrade gaps.

The Calculated Reality: Waiting for a catastrophic 30% price correction in a heavily regulated, supply-constrained market is a statistical improbability. A Calculated Entry Strategy demands that you divorce your timeline from retail market noise. You must execute your transition based strictly on your personal capital readiness and structural market data, not on fear, hype, or speculative hope.

10.1 Waiting Forever for a Big Crash

- You keep hoping for a 20–30% crash "like last time," but it may never come in the same way.

- As you saw earlier (PropNex base-case: private + HDB resale projected +3% to +4% in 2026), the market is more 'stable/normalising' than 'panic/crash'.

- Meanwhile, your rent, replacement cost, and life plans (kids, parents, retirement) keep moving on without you.

10.2 Only Buying When It Feels "Dirt Cheap"

- You reject fair-value deals because they don't feel like a "steal."

- In a mature, land-scarce market like Singapore, truly "dirt cheap" is rare—and often comes with a catch: weak demand, poor layout, or a problem location.

10.3 Over-Analysing Until Nothing Happens

- You read every article, watch every video, run every scenario... but never commit.

- By the time you're "finally certain," the good units are gone or have moved to a different price band.

How to Counter These Traps

- Set clear rules upfront—your safe band, buffer, and minimum holding period (e.g., 4–7 years).

- Use Scenario A vs Scenario B thinking, not just "wait and see." For example, compare "Wait 3–5 years" vs "Use this 2026 window" using your own numbers.

- Decide in advance what makes you say "yes" or "no"—so you're not swayed only by fear, hype, or the latest headline.

Once your numbers and rules are clear, the goal is not to time the perfect bottom.

The goal is to make a calm, grown-up decision you won't regret five to ten years from now.

Understanding your own psychology is as important as understanding the market.

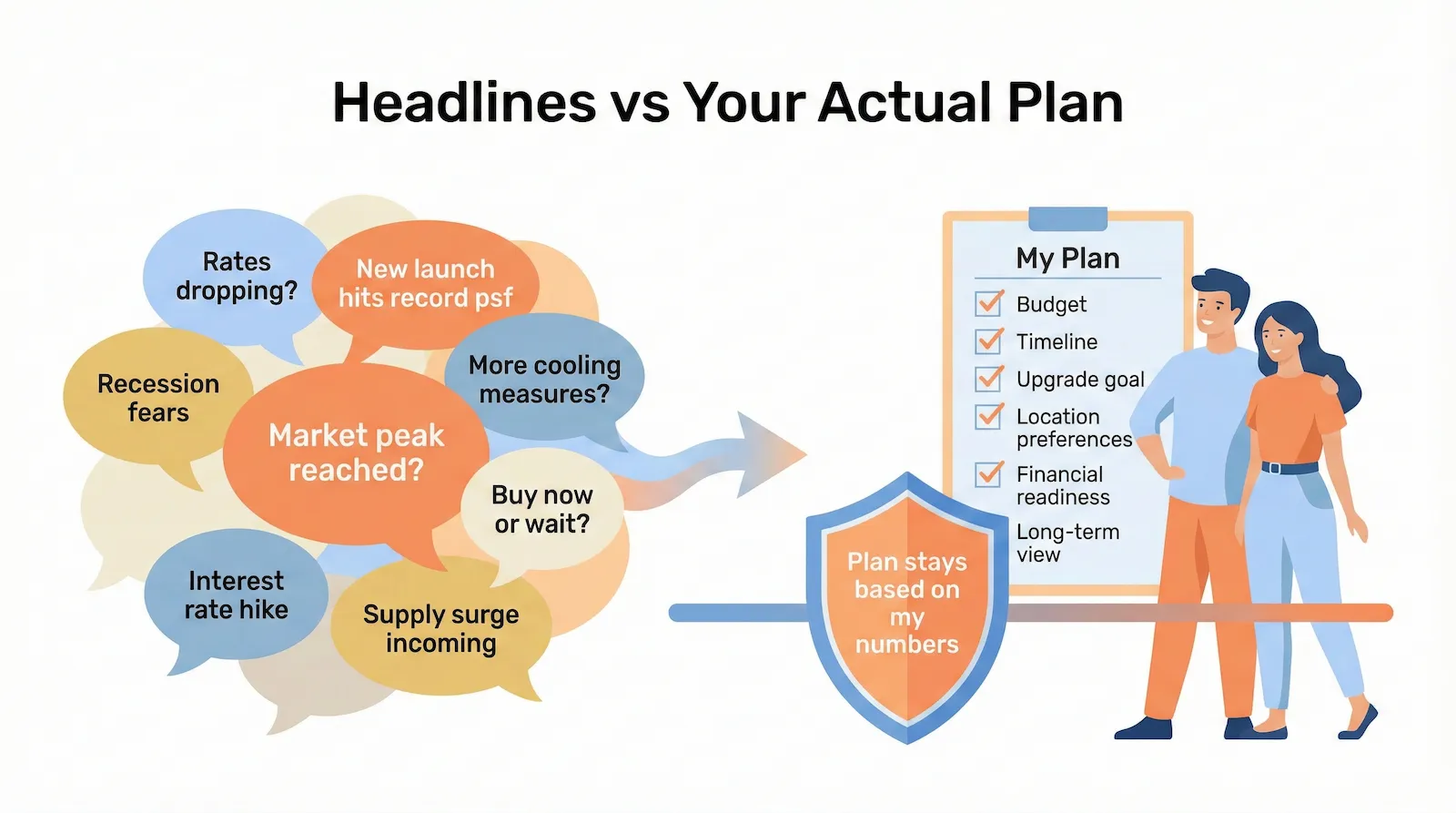

10.4 Headlines vs Your Actual Plan

If you only follow headlines, your emotions will be all over the place:

One month: "Rates high, cannot buy now."

Next month: "Rates dropping, faster grab."

Next quarter: "Recession scare, better wait."

Next year: "New launch record price, too late already."

The news cycle will always find a way to make you feel either scared or left out.

What actually matters more than the headlines are two things:

- The big structural forces we talked about earlier—land cost reset, HDB double wave, supply, and money rotating from stocks into property.

- Your own default behavior under uncertainty—do you freeze, chase, or drag until opportunities pass?

Once you're aware of your own pattern, you can design a plan that follows your numbers and timeline, not this week's headline.

Headlines can be noisy. Your plan should follow your numbers and timeline, not every news alert.

In the next section, you'll see how three different buyers used these ideas to make real decisions in this 2026 window.

11. 2026 Decision Case Studies: HDB, First-Home, Second-Property

Theoretical frameworks only possess value when applied to actual market conditions. The following models demonstrate how to execute a Calculated Entry Strategy across different buyer profiles within the current crossover window.

The Calculated Reality: Whether executing an HDB transition, an initial private property acquisition, or an investment deployment, the mathematical fundamentals remain identical. These case studies illustrate how to lock in an entry price, structure the requisite capital buffers, and establish a clear exit timeline without succumbing to retail market panic or over-leverage.

11.1 Sengkang Couple, Mid-40s, Two Kids — Upgrade Scenario

- Current: 4-room HDB in Sengkang, remaining lease healthy.

- Both working, combined income about $14k/month.

- Considering a 3-bedder OCR condo near parents to help with childcare.

After going through the financing safety nets (Section 9):

- Housing ratio at new condo: ≈ 33% at current rates; still below 40% even at +2% interest.

- Buffer: about 9 months of essential expenses after the move.

- Scenario A – Wait 3–5 years:

– Risk MOP wave adding more HDB supply in their town.

– New land cost pushing future launch prices higher. - Scenario B – Use the 2026 window:

– Lock in today's HDB gains while resale is still firm.

– Buy into a sensibly priced old-land project with a 7–10 year horizon.

They decide to move this cycle, but not anyhow buy. They shortlist only projects that:

- Have decent school access and family-friendly layouts;

- Are not at the very top end of the price range;

- Let them hold comfortably for at least one full cycle.

Key takeaway: Once the maths and buffers are clear, the real question becomes:

"Do we use this window or wait on purpose?"

—not "Can we guess the exact market top?"

If the new-launch entry quantum strains their safe band, the Park Colonial resale at Woodleigh is the natural NEL-corridor comparable to benchmark against — one stop closer to the city on the same train line, at a different price baseline from the 2026 new-launch wave.

On the same Woodleigh MRT station, The Woodleigh Residences at Bidadari Park Drive is the integrated-development comparable — Kajima × Singapore Press Holdings, 667 units with direct Basement 2 access to Woodleigh MRT (NE11) and the underground bus interchange, sitting on the Bidadari estate frontage. Two NEL-corridor reads to benchmark against — Park Colonial as the standalone resale, Woodleigh Residences as the integrated resale — across two distinct entry quanta on the same upgrader train line.

Map your specific HDB-to-condo timeline before listing or booking — the HDB-to-condo timeline calculator walks through the sell-first vs buy-first sequencing.

11.2 Renting Near CBD, Early 30s — First-Home Scenario

- Renting a 1-bedder near the CBD at about $3,500/month.

- Combined income around $11k, with decent savings and CPF.

- Feels that "prices already so high... Maybe it's better to wait first."

After going through the financing safety nets (Section 9):

- They realize they can comfortably buy a $1.6–1.7M OCR/RCR 2-bedder, with a housing ratio of ~34% and about 10 months' buffer after all costs.

- They shortlist a mix of resale and new launches, focusing on:

– Layout that works for 5–7 years, not just 1–2;

– Reasonable commute and everyday convenience;

– Unit types with real future demand (not hyper-niche layouts).

They decide to stop paying high rent and commit to a home that fits their numbers, instead of waiting indefinitely for a "perfect" crash that may never come.

Key takeaway: They don't try to time the bottom.

They avoid overstretching, buy a sensible, liveable unit, and start building equity instead of just funding the landlord's mortgage.

If you're working through your own first-home math, the Gap Decoder affordability calculator stress-tests your safe band before you start viewing.

11.3 Second-Property Scenario: One Existing Home Plus ABSD

- Owns a fully paid 3-bedder in the East, staying there with family.

- Considering a second property in the RCR, but will incur ABSD and have a tight buffer.

Using the Investor Pre-Commit Checklist (Section 7.1):

- Entry price & rental demand:

– Purchase price and expected rent look reasonable compared to nearby resale. - But two red flags appear:

– Buffer is thin – if rent dips or the unit is vacant for a few months, monthly cashflow will be very stretched.

– Exit clarity is weak—they can't clearly answer, "Who will buy this from me in 7–10 years, and why at my target price?"

Instead of forcing the purchase just because "2026 is a good window," they decide to:

- Build up more buffer over the next 2–3 years;

- Consider restructuring their existing position first (for example, right-sizing their home, then planning an investment);

- Revisit an investment purchase only when all four investor boxes are "yes."

Key takeaway: Sometimes the best decision in a good window is still to wait intentionally with a clear plan. Rather than push through a borderline investment just for the sake of "doing something."

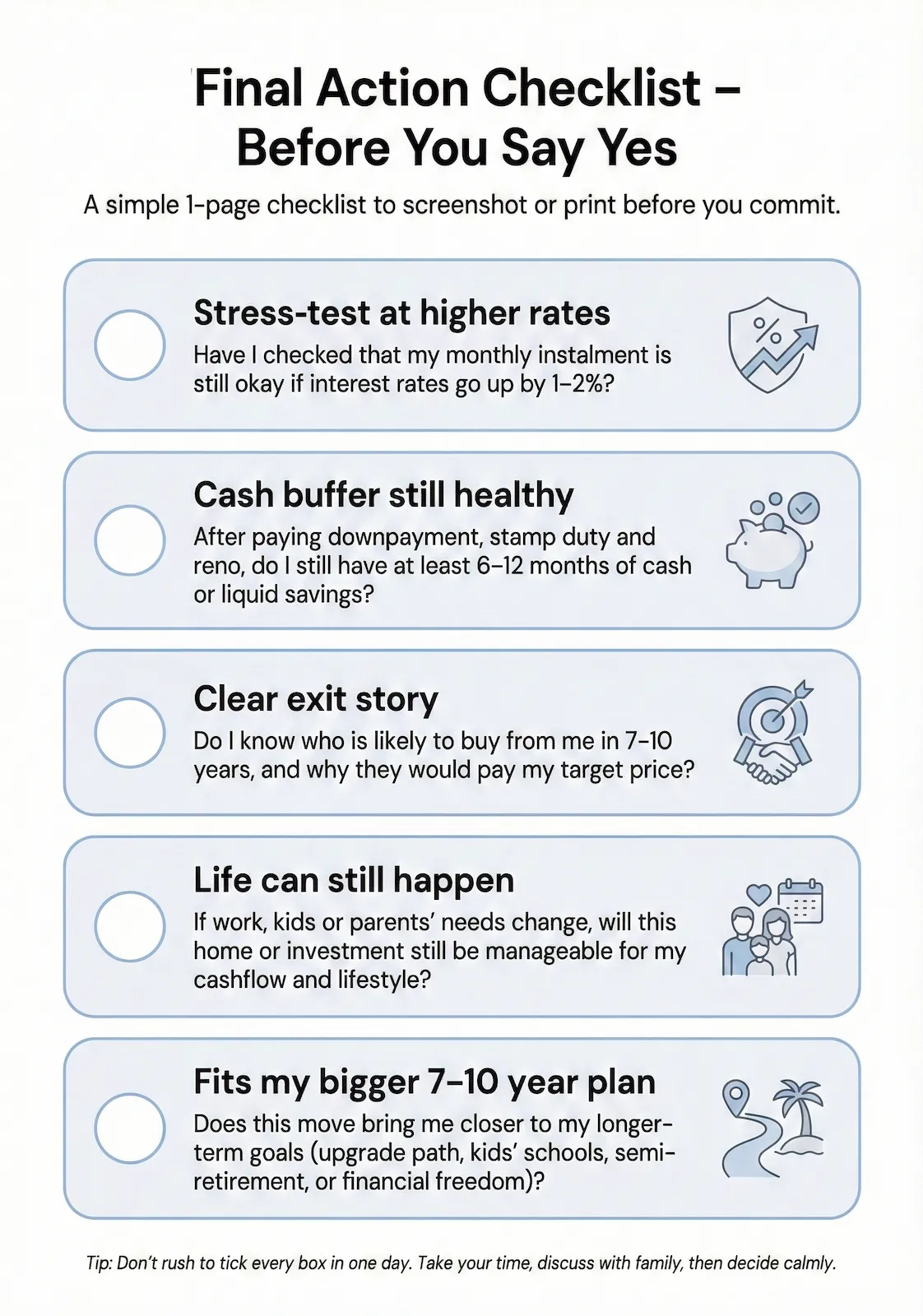

"Final Action Checklist—Before You Say Yes"

By now, you probably have a clearer sense of where the market is, what kind of buyer you are, and what options are realistic for your budget. The last step is very simple: slow down a bit, and run through a short checklist before you say "yes." It's better to take one more night to think than to rush into a 7–10 year commitment.

Below is a 1-page action checklist you can screenshot or print. Use it as a quiet filter with your spouse or family. If you can confidently tick every box—stress test, buffer, exit story, life flexibility, and long-term plan—then you're not just buying because the headlines say "window." You're buying because it fits your numbers, your season of life, and your bigger goals.

A simple 1-page action checklist. Screenshot or print this and tick every box before you say "yes."

Why this checklist matters: In Singapore, the market can stay firm even when headlines turn noisy—because policy guardrails and real demand reduce "wild swing" behaviour.

So the goal isn't to predict the next headline. The goal is to make sure your numbers, buffers, and holding power are strong enough to ride through normal volatility.

If you can calmly tick these boxes, you're deciding based on a plan, not vibes.

Once you've gone through that checklist, the final section is simply about how we can sit down, run your numbers properly, and decide whether now is the right window for you—calmly, without pressure.

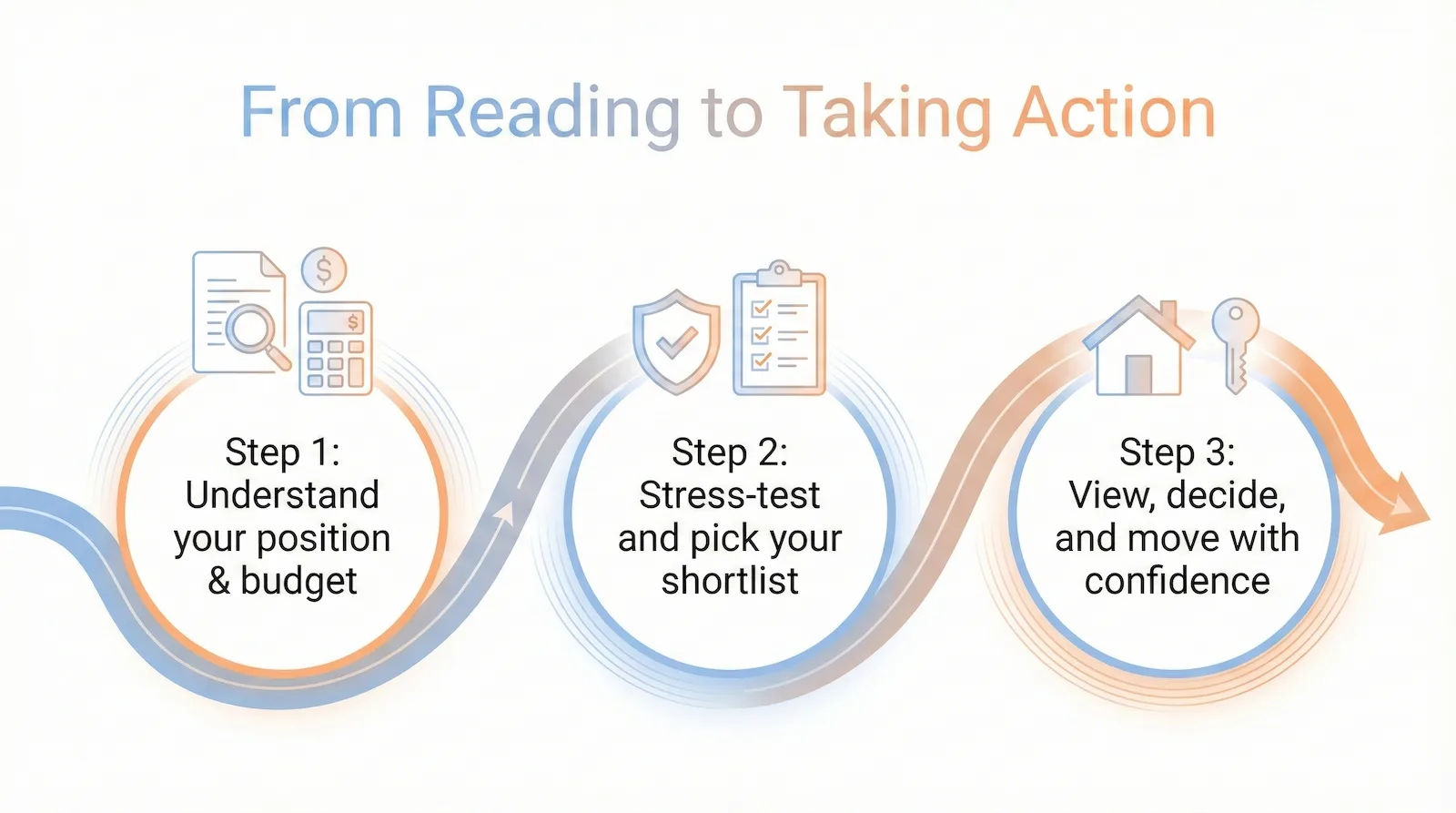

12. From Reading to Taking Action: Your Next Steps

Macroeconomic data is useless without a micro-level application to your personal balance sheet. The objective of this blueprint is to transition you from passive observation to calculated, data-driven execution.

The Calculated Reality: The next step is a rigorous, 1-on-1 Portfolio Architecture Session. We will mathematically map your current equity, calculate your exact upgrade gap, stress-test your capital against current SORA rates, and identify specific 'old land' opportunities that align with your 5-7 year exit strategy. We engineer the mathematics; you make the final decision.

12.1 What We Can Do Together

When we sit down together, we'll usually go through three stages:

1) Map your position

- For HDB owners—estimate your likely sale price, net proceeds, and upgrade gap.

- For condo owners—review your current position, equity, and options (hold, right-size, or progress).

- For renters/first-timers—work out a safe budget, cash/CPF position, and key trade-offs.

- For investors—review your portfolio, loan capacity, and risk appetite.

2) Stress-test and shortlist

- Run your financing numbers with a banker at today's rates and at +1–2%.

- Shortlist a mix of new launch and resale options that truly fit your comfort zone.

- Use the 2026 window to your advantage, instead of letting headlines scare you.

3) View, decide, and move with confidence

- Visit the right projects (not every project).

- Compare layouts, facing, and future demand on site.

- Decide based on a calm, structured plan—not hype or FOMO.

A calm, structured process helps you make confident decisions in the 2026 window.

The goal is not to rush you into buying.

The goal is to help you make a conscious decision—whether that's "move this cycle" or "wait on purpose with a clear plan."

12.2 About Sam

My name is Sam Tan. I run Dunamis Property and am a registered real estate salesperson with PropNex Realty Pte Ltd. My focus is:

- HDB upgraders moving into the private condo market

- First-time condo buyers and condo upgraders

- Residential property investors who want clarity, not hype

CEA Registration: R060444I

Brand: Dunamis Property (PropNex Realty Pte Ltd)

Contact: 9108 0880

Website: https://dunamisproperty.com.sg

12.3 How I Can Help You

If you found this guide useful and want a conversation that's specific to your situation, here are three simple options:

"Upgrader Window" consultation

We map out your HDB position, likely sale price, net proceeds and upgrade gap, then compare Scenario A (wait) vs Scenario B (move this cycle) using real numbers. This helps you see clearly how your upgrade gap might change under different paths.

First-time / condo upgrader planning session

We work through your income, savings, comfort band and time horizon, then build a shortlist of projects and unit types that truly fit your budget — not just dream projects. The aim is a home you can hold comfortably for 5–7 years, not a stressful 1–2 year flip.

Investor clarity call

We stress-test your numbers, review locations and unit types, and see whether an investment unit really makes sense for you right now. Sometimes the best outcome is "wait and strengthen first" — and that's a perfectly good result.

When you reach out, just mention this guide. I'll know you've already done your homework, so we can go straight into your numbers, scenarios and next steps — not spend the session repeating what you've already read.

No hard sell, no pressure. Just a calm, structured conversation to help you decide whether to use this 2026 window — or to wait on purpose with a clear plan.

Glossary – Key Terms in This Guide

A quick reference for common terms and acronyms used in this guide.

ABSD – Additional Buyer's Stamp Duty

A tax paid on top of normal Buyer's Stamp Duty when you buy additional properties or certain types of residential property. Designed to discourage speculative buying and "anyhow buy a few units" behaviour.

BTO – Build-To-Order flat

New HDB flats launched by the government, usually with a 5-year Minimum Occupation Period (MOP) before you can sell on the resale market.

Buffer/Emergency Buffer

Cash or very safe savings you keep aside for emergencies. In this guide, we usually talk about 6–12 months of essential expenses as a healthy buffer after you've paid all buying costs.

CCR – Core Central Region

The "prime" city areas of Singapore (e.g. Orchard, CBD, some parts of Bukit Timah). Traditionally the most expensive region for private condos.

Cooling measures

Policies the government introduces to slow the market when prices or activity run too hot, such as tighter loan rules or higher stamp duties. They don't freeze prices completely, but they reduce extremes.

Double Wave (HDB "Double Wave")

A term used in this guide to describe two things happening together:

1. Wave 1: Strong HDB price gains over the last cycle.

2. Wave 2: A large batch of newer BTO flats reaching MOP from 2026–2028, adding more resale supply.

Together, they affect both HDB prices and the upgrade gap to condos.

GLS – Government Land Sales

Land sites released by the government and sold to developers through tenders. The GLS land cost (psf ppr) becomes a key backbone for future launch prices.

HDB – Housing & Development Board flat

Public housing flats where a large majority of Singaporeans live. In this guide, "HDB upgrader" usually means a household selling an HDB to move into a private condo.

Housing ratio

Your total monthly housing costs (loan instalment + basic running costs) divided by your gross household income. A common comfort band in this guide is around 35–40% or below, not as a strict rule but as a safe reference.

Land bank

The stock of undeveloped land sites a developer already owns. When land banks are low, developers must bid more actively for new GLS sites to secure future projects.

Land cost (psf ppr)

The price a developer pays for land, measured per square foot per plot ratio (psf ppr). Higher land cost usually means higher eventual launch prices for that project or area.

Launch price

The psf price that new-launch units are sold at when a project first comes to market. In this guide we often compare older "old-land" launch prices vs future "new-land" launch bands.

MOP – Minimum Occupation Period

The minimum number of years (usually 5) you must live in your HDB flat before you can sell it or buy certain private properties. A large batch of flats reaching MOP can create a "wave" of resale supply.

OCR – Outside Central Region

Heartland areas further from the traditional city core. Often called "mass-market" condos—but newer OCR land costs mean future launches may not feel cheap compared to past cycles.

PPI – Property Price Index

The URA index that tracks overall private home prices across Singapore. In this guide it is used to show that prices tend to correct and move sideways, but rarely crash 20–30% in one shot.

psf – Per square foot

A common way to quote property prices in Singapore. For example, a condo at $2,200 psf means $2,200 per square foot of strata area.

psf ppr – Per square foot per plot ratio

Used mainly for land bids. It reflects the land price per square foot of potential buildable floor area after applying the plot ratio.

RCR – Rest of Central Region

City-fringe locations just outside the prime CCR. Recent GLS tenders show RCR land costs moving closer to CCR levels, which is why future RCR launches may be priced much nearer to traditional "prime" pricing.

SSD – Seller's Stamp Duty

A tax payable if you sell a residential property within the first 4 years after purchase. It encourages longer holding periods and reduces quick flips.

Stress-test (interest rate stress-test)

Checking your monthly loan instalment at 1–2 percentage points above your starting interest rate, to see if you can still hold comfortably without panic selling.

TDSR – Total Debt Servicing Ratio

A rule that caps your total monthly debt repayments as a percentage of income. It prevents buyers from over-leveraging even if they feel they can stretch more.

Unsold inventory

Units in launched projects that are still unsold. When unsold inventory is low and land banks are thin, it is harder for prices to drop sharply unless there is a major shock.

Upgrader (HDB or condo upgrader)

A buyer moving from a current home (HDB or private) to a better or more suitable property—usually with a bigger budget and higher expectations for space, location or lifestyle.

"Window" (2026 window)

In this guide, the 2026 window refers to a 12–24 month repositioning period where:

• Old-land projects are still selling.

• New-land GLS sites are setting higher future price bands, and

• The HDB double wave is playing out.

It's not predicted as a "crash year", but as a key timing window to decide whether to move, restructure, or wait on purpose with a clear plan.

DISCLAIMER

While every reasonable care is taken to position the accuracy of

information printed or presented here,

no responsibility can be accepted for any loss or inconvenience

caused by any error or omission.

The ideas, suggestions, general principles,

examples and other information presented here are

for reference and educational purposes only.

This presentation is not in any way intended to

provide investment advice or recommendations to buy,

sell or lease properties or any form of property investment.

PropNex shall have no liability for any loss or expense

whatsoever relating to investment decisions made by the audience.

You shall fully indemnify us against any damage, loss or expense

whatsoever arising directly or indirectly as a result of any

actions taken based on this guide.

Original Research

The Two Clocks Problem: Why New Launch Prices Lift Leasehold Value

Your 99-year lease ticks down every year — but new launch prices nearby keep pulling resale values up. Here is what 30 years of data actually show, and why the popular lease-decay forecasts get it wrong.

Read the AnalysisDecision Tools

Run the Numbers Before You Decide

Three free calculators. No sign-up. Decode your affordability, cashflow, and transition in sequence.

Can I Afford This Condo?

Stress-test your TDSR, minimum cash, and ABSD before you commit.

Open CalculatorWhen Do I Pay What?

Map your progressive payment schedule for new launch condos.

Model CashflowSell HDB or Buy Condo First?

Time your transition to avoid ABSD and bridging loan exposure.

Open MatrixSpeak Directly With the Founders.

Many of our clients prefer an immediate, private conversation to discuss their portfolio. Tap below to connect directly with Sam and Lisa to strategise your next move.

Frequently Asked Questions

2026 Singapore Property Buying FAQ: Transition Window, Affordability & Upgrading

2026 is a transition window rather than a 'cheap' or 'crash' year. The math anchors to old-land launches still selling, new-land GLS sites setting higher future benchmarks, and the HDB MOP supply wave unfolding from 2026 to 2028. Whether it's a good time for you depends on your specific housing ratio, buffer, and 7-10 year holding plan — not on predicting a market bottom that may not arrive.

Singapore private home prices have historically corrected and moved sideways through AFC, SARS, GFC and successive cooling measures without a 20-30% reset. Policy guardrails (TDSR, ABSD, SSD) filter out speculative buying and reduce forced-selling pressure. PropNex's base case projects private and HDB resale prices both at roughly +3-4% in 2026. A sudden catastrophic crash in a regulated, supply-constrained market is a statistical improbability — though individual projects can still correct based on specific fundamentals.

Waiting for a 20-30% crash is less a decision than a postponed decision. The cleaner framework is Scenario A (wait 3-5 years) vs Scenario B (use the 2026 window), each with specific numbers: your HDB resale projection against the MOP supply wave, your target condo price against new-land GLS benchmarks, and your monthly instalment stress-tested at +1 to +2 percentage points. Run both scenarios through the Gap Decoder affordability calculator before committing either way.

There's no single income figure — the math depends on your target property, downpayment, and comfort band. Two reference points: keep total housing costs (instalment plus running costs) below 35-40% of gross household income, and preserve 6-12 months of essential expenses as liquid buffer after all acquisition costs. As a worked example, Chapter 11.2 walks through an early-30s first-home buyer on ~$11k combined income buying a $1.6-1.7M 2-bedder with a ~34% housing ratio and ~10 months' buffer.